You’re Overpaying—Here’s the Actually Low-Life Living Trust Cost

Ever landed on a trusted finance page only to find trust fund fees feel surprisingly high? With rising cost-of-living pressures and growing awareness of financial tools, more US readers are asking: “Am I paying more than I need to for a living trust?” The short answer: yes, for many. This article unpacks why current trust structures often carry more expense than necessary—without sensationalism—helping you understand where overpayment comes from, how it works quietly beneath the surface, and whether it’s truly worth the cost. From $10K+ To $2K×Unlock The Living Trust Cost Hack

Right now, a shift is underway. Rising inflation, shifting estate planning expectations, and a new wave of transparency around legacy costs have sparked widespread curiosity. People are no longer accepting opaque trust fees blindly—especially when simpler, lower-cost options exist. This isn’t just trend speculation; it’s a measurable recalibration driven by informed, mobile-first consumers seeking clarity and value.

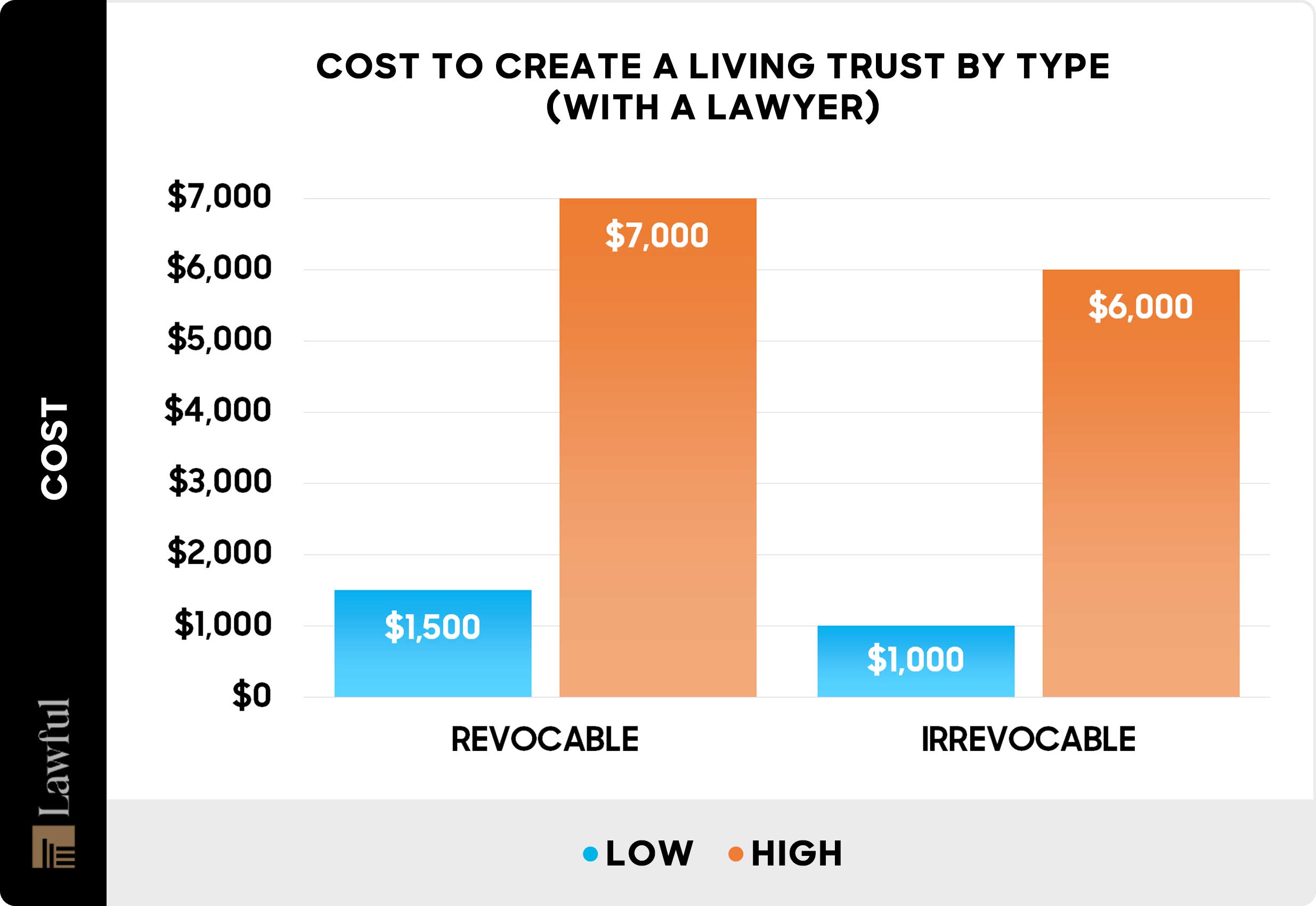

Living trusts are often framed as essential for estate protection, but the reality is more nuanced. From $10K+ To $2K×Unlock The Living Trust Cost Hack Traditional trust structures—specifically revocable and certain asset-protected trusts—tend to carry high administrative, legal, and ongoing maintenance fees. Many providers price these services around $200–$600 monthly, often without clear justification, even when life’s actual risks are minimal. This disconnect between expected necessity and actual cost is what fuels the “overpaying” perception.

But here’s the key: not all trusts come with a steep price tag. The actual low-life cost of secure, basic living trusts typically ranges from $75 to $150 per month—accessible even on tight budgets. From $10K+ To $2K×Unlock The Living Trust Cost Hack The premium often stems from outdated fee models, redundant services, and complex structures users don’t need. By cutting unnecessary layers—like third-party monitoring or premium estate planning bundles—true cost efficiency becomes achievable.

If you’re already paying more, understanding why reveals a clear pattern: generic pricing, lack of transparency, and over-engineered solutions disproportionately inflate expenses. No one’s being taken for a ride—but many are unknowingly paying inflated fees for minimal protection.

For some, especially those without high-value assets or complex family setups, the full trust might feel unnecessary. Others require formal protection but can avoid hidden markups by choosing streamlined plans with minimal overhead. Mobile users, scanning quick insights on tight screens, value straightforward, no-nonsense cost evaluation—without fluff.

If you’re reexamining your trust arrangement, this isn’t a call to eliminate legacy planning. It’s a prompt to check alignment: Are your fees proportional to actual risk and control? When trusted providers offer clear, flexible trust structures at $100 flat or less, that’s a strong sign. Scrolling deeper means you’re not overpaying—you’re investing wisely.

Still on the fence? Consider: lower fees today mean more control over your estate for fewer decades. The actual low-life cost isn’t about risk—it’s about smart resource allocation. With updated models and greater transparency, living trusts can be both protective and affordable.

Ultimately, informed choice matters more than fear-driven outrage. As you navigate this trend, focus on clarity, affordability, and real value—not just headlines. Your trust doesn’t need to cost an arm and a leg to serve its purpose.

Take control. Explore, compare, and stay educated. Your estate planning future deserves honesty—and today’s market offers tools that deliver on both security and savings.

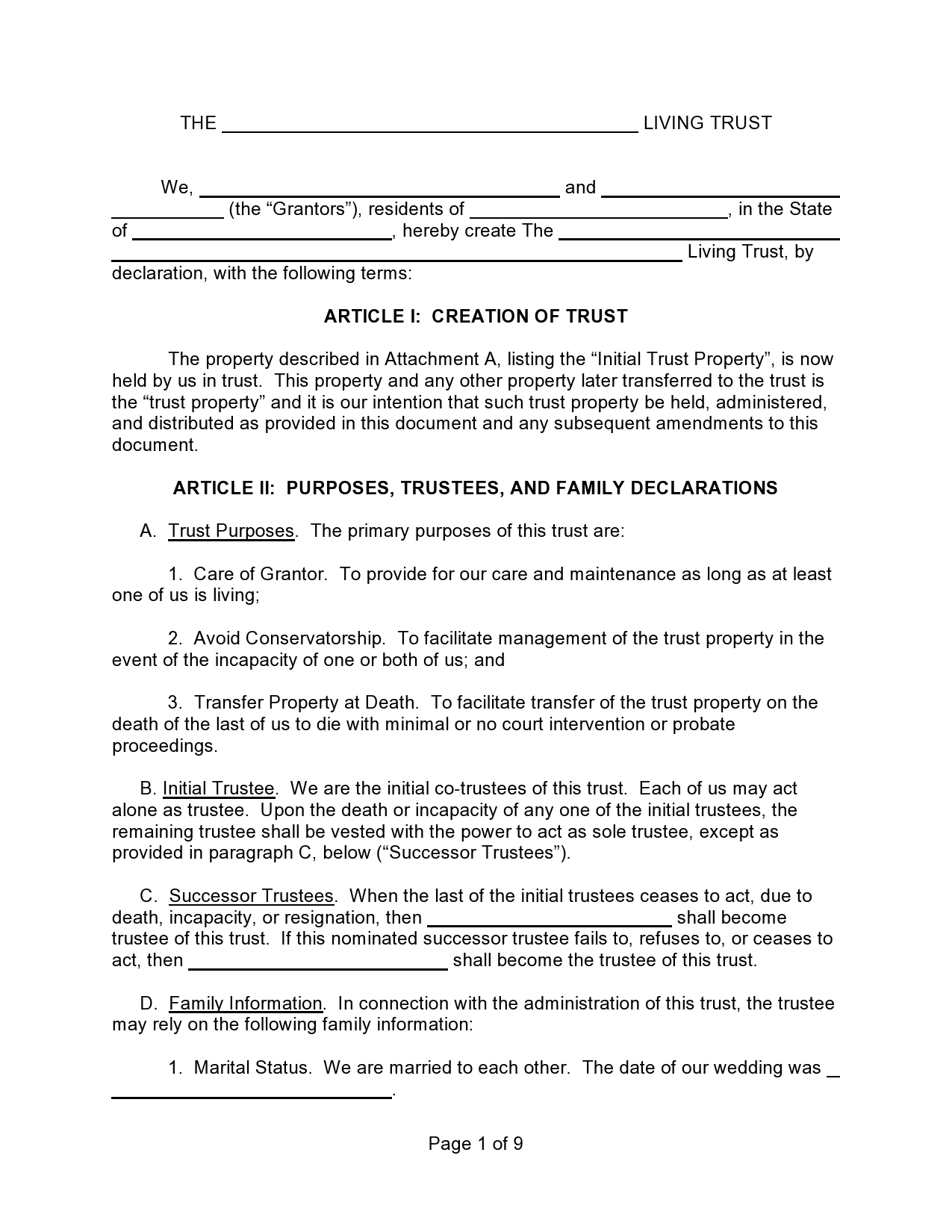

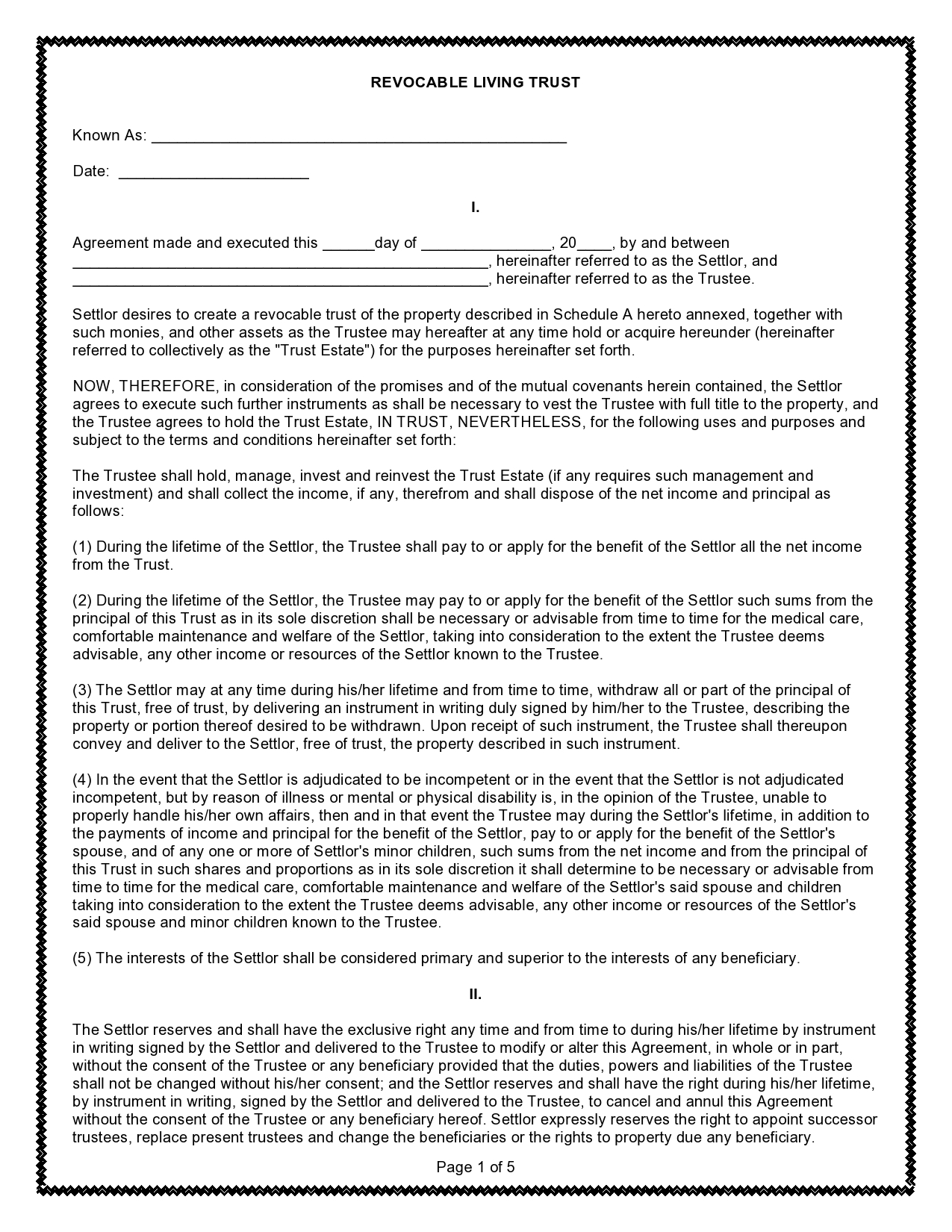

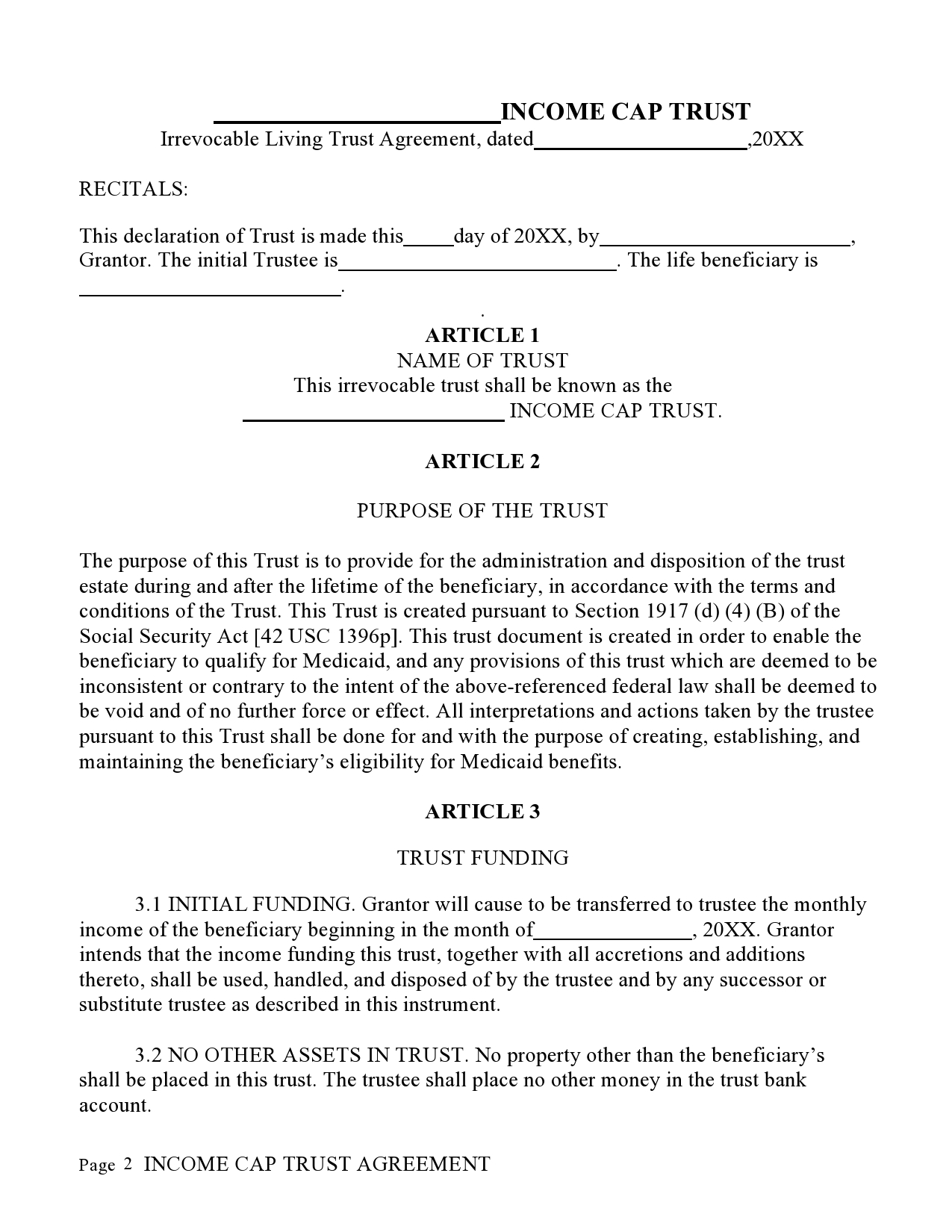

![Free Printable Living Trust Templates [PDF] Irrevocable](https://www.typecalendar.com/wp-content/uploads/2023/06/Blank-Form-of-Revocable-Living-Trust.jpg)