The Plano Rent-to-Own Hook: Turn Rent Into Your First Home Fast

What if putting a down payment aside could become a step toward homeownership in under a year? In cities like Plano, Texas—and across many U.S. markets—this idea is sparking growing interest. The Plano Rent-to-Own Hook: Turn Rent Into Your First Home Fast is more than a catchy phrase—it’s a practical path many are exploring to build equity quickly while navigating higher housing costs. Plano Rent-to-Own Homes Under $400K×Opportunity Knocks

As housing prices rise and traditional buying timelines stretch longer, renters are increasingly drawn to structured rent-to-own models that blend flexibility with real progress toward owning. This trend reflects a shifting mindset: long-term financial planning now includes smarter, phased entry points into homeownership, where rent payments grow into equity with minimal upfront cost.

Understanding How the Plano Rent-to-Own System Works

The Plano Rent-to-Own program allows eligible renters to lease an apartment with a portion of monthly payments applied directly toward a future home purchase. When enrolled, a percentage—typically 10–20%—of each rent is recorded as credit toward the down payment. This creates a transparent, measured way to save toward ownership without immediate large financing. Plug In Now: Plano Rent-to-Own Homes Tsunami Expected Plano Rent-to-Own Homes Under $400K×Opportunity Knocks

The process is straightforward: tenants pay standard rent, but agreements outline clear milestones—such as credit score thresholds, savings goals, or rental tenure—after which some or all accumulated payments convert into an equity deposit. This structured approach reduces financial surprises and aligns with long-term budgeting habits, making it accessible for first-time buyers navigating uncertain market conditions.

Common Questions About Rent-to-Own in Plano

Q: Do I actually own anything during rent-to-own? A: Yes. Accumulated payments build documented equity over time, which acts as a down payment deposit when finalizing a mortgage. Plano Rent-to-Own Homes Under $400K×Opportunity Knocks You don’t own the leased unit long-term, but the program treats your rent as invested capital.

Q: What credit requirements are needed? How To Score Plano Rent-to-Own Homes Before They're Gone A: Most plans require a minimum credit score (usually 620+), proof of stable income, and a clean rental history. These criteria help protect both tenant and program integrity.

Q: Can I use this to rent in Plano? A: The program is available through select property management firms and real estate platforms registered in Texas. Eligibility may vary by landlord, but rising adoption suggests growing accessibility.

Q: Does paying rent count toward ownership immediately? A: Partially. Rent contributions are tracked and applied to future ownership, but upfront legal title doesn’t transfer until full enrollment and fulfillment of program terms.

Opportunities and Realistic Expectations

The appeal lies in speed, structure, and affordability. Unlike traditional mortgages, which demand large deposits and credit checks early, rent-to-own lets budgeting beginners begin saving without high-pressure financing. With clear milestones, it promotes financial discipline and transparency.

However, this path isn’t fast-forward ownership. Market fluctuations, income changes, and credit updates can affect progress timelines. Users must remain engaged, meeting periodic requirements to maintain momentum. That said, for many, this phased approach offers genuine opportunity—not just a speedy shortcut—building confidence and financial footing.

Common Misconceptions and Clarifications

Myth: I lose control of my rent payments. Reality: You continue paying market-rate rent. The program adds a small equity component—not a separate burden.

Myth: Rent-to-own guarantees homeownership. Reality: Success depends on meeting internal program criteria and housing market conditions. It’s a tool, not a guaranteed outcome.

Myth: All renters qualify instantly. Reality: Each program has tailored criteria, including income stability, rental history, and approval checks. Not every renter enters automatically.

These distinctions help manage expectations while reinforcing the program’s role as a flexible, accountable tool—not a universal solution.

Who Benefits from the Plano Rent-to-Own Approach?

This strategy suits diverse groups: first-time buyers eager to build equity with minimal risk, young professionals stabilizing careers while planning long-term housing, investors testing markets with low initial commitments, and renters seeking gradual financial growth without high-pressure financing. Its neutral design ensures accessibility across income levels and life stages, avoiding one-size-fits-all assumptions.

Embracing the Plano Rent-to-Own Path Softly

The Plano Rent-to-Own Hook: Turn Rent Into Your First Home Fast reflects a broader U.S. shift toward smarter, incremental homeownership. In a climate where rent often outpaces income gains, this model offers real value—transparency, measurable progress, and personal control. For those curious, the option invites exploration rather than pressure. With thoughtful planning and realistic expectations, users can turn monthly rent into a tangible step toward stable, owned shelter.

Stay informed, assess your own path, and view this tool as part of a thoughtful journey—not a quick fix. The future of homeownership in Plano and beyond may be leasing with purpose.

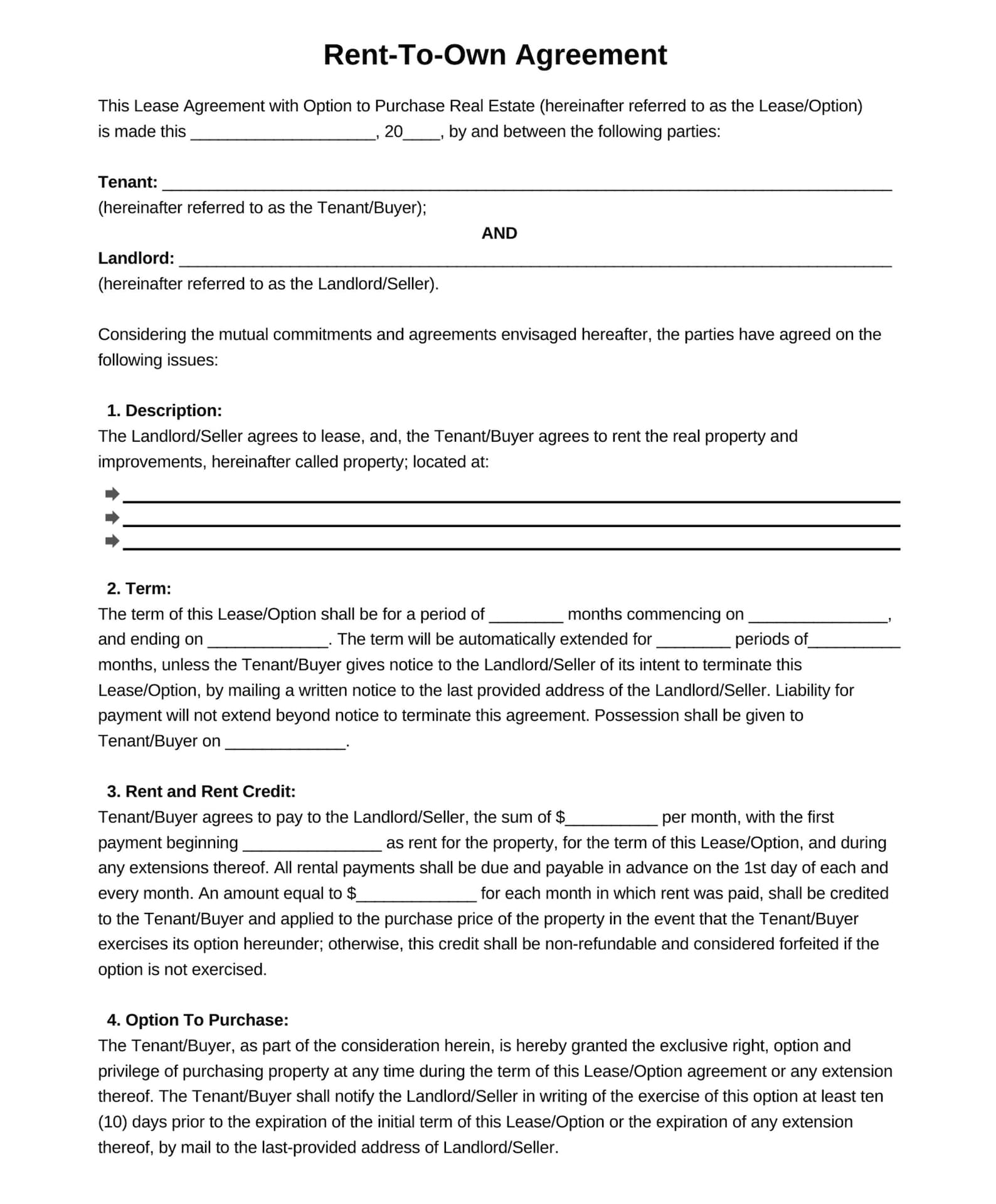

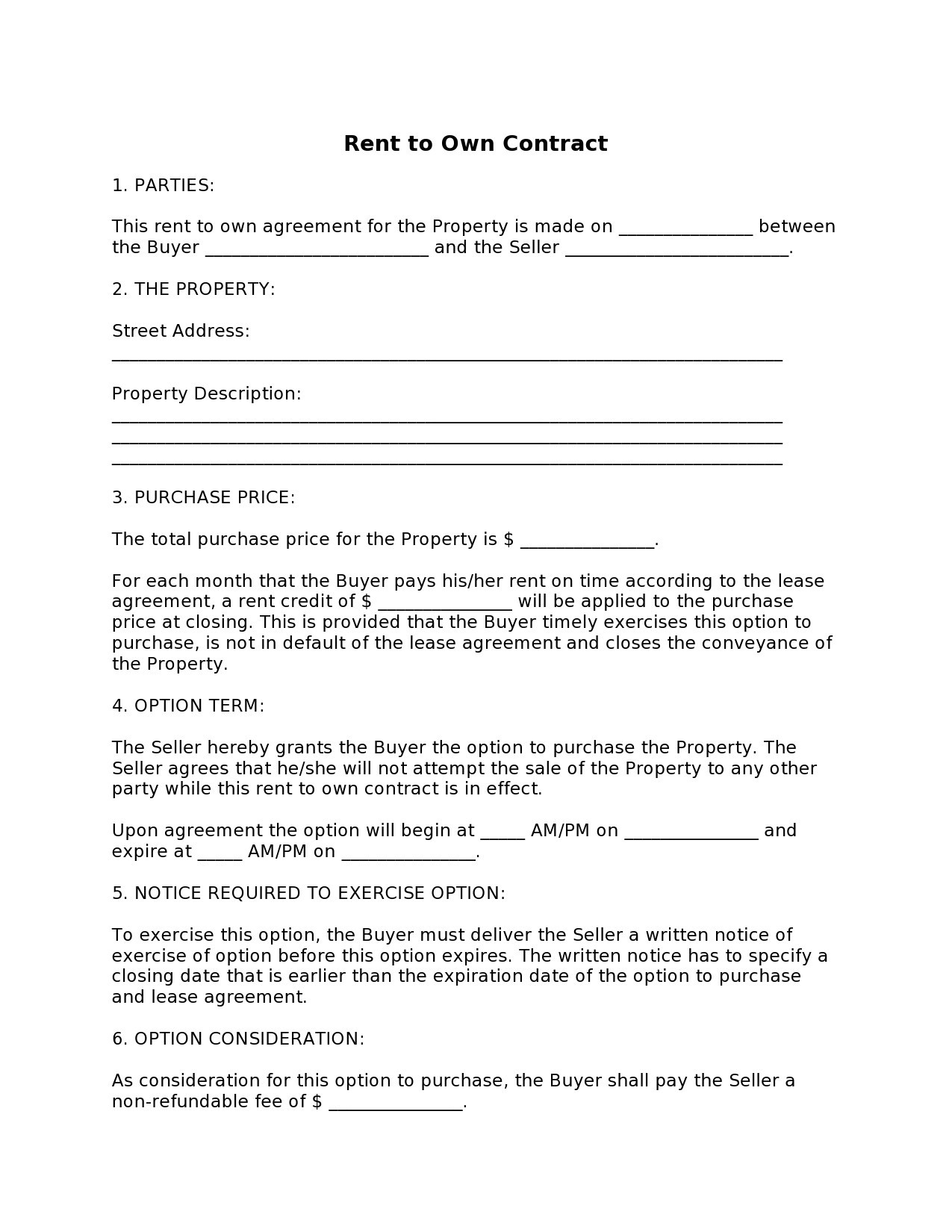

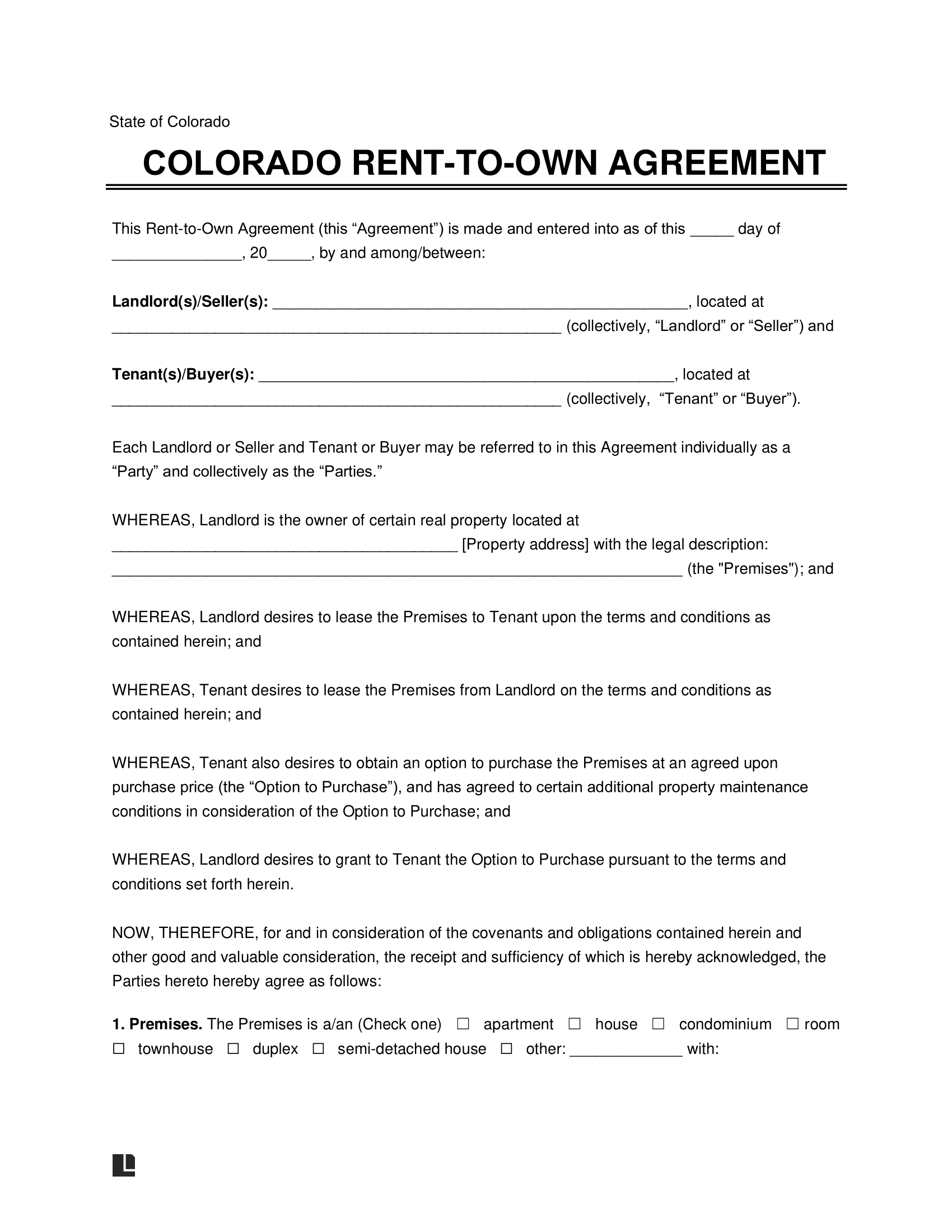

![Free Printable Rent To Own Contract Templates [PDF, Word] Vehicle, Car](https://www.typecalendar.com/wp-content/uploads/2023/05/rent-to-own-agreement-template.jpg)