The Mandatory Direct Deposit Rule Every Employee Silently Follows

People across the U.S. are quietly adapting to a workplace finance shift that’s reshaping how employees manage payroll—without most even realizing it. At the center of this shift is the Mandatory Direct Deposit Rule Every Employee Silently Follows. Though rarely discussed in casual conversation, this policy quietly governs a major part of modern employment stability, influencing budgeting habits, bank relationships, and financial peace of mind. Mandatory Direct Deposit: The Hidden Law Organizing Every Payday As remote work and gig economy growth persist, this silent rule is becoming not just common, but essential to understand.

Why is direct deposit—the automatic transfer of wages straight to bank accounts—so deeply embedded in daily financial life? Unlike cash or paper checks, direct deposit ensures timely, secure access to income. The rule governing its use has tightened over time, creating an unspoken but powerful expectation: employees rely on deposits arriving exactly when owed, with minimal disruption. This consistency supports budgeting reliability, especially amid economic uncertainty where income timing impacts everything from rent payments to credit health. Mandatory Direct Deposit: The Hidden Law Organizing Every Payday

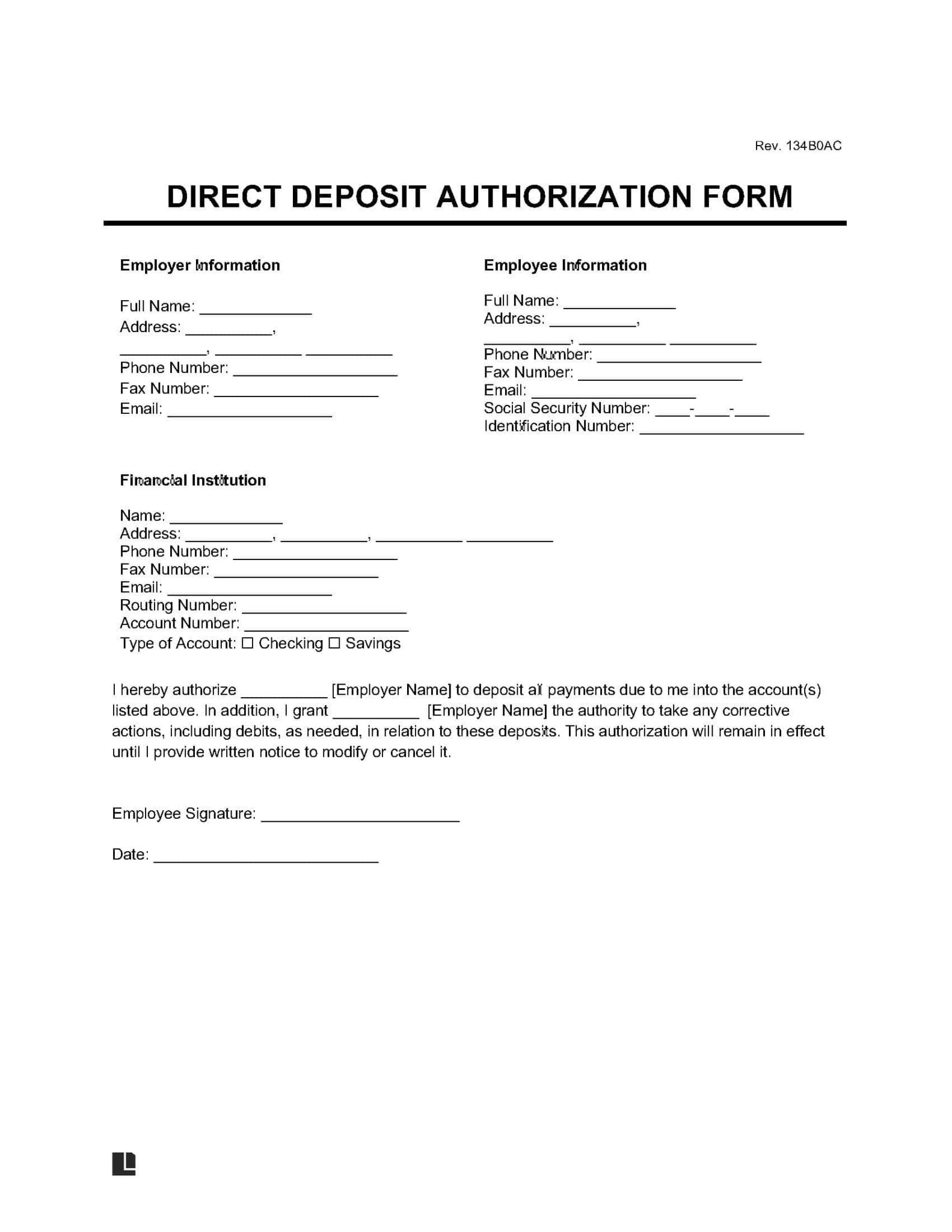

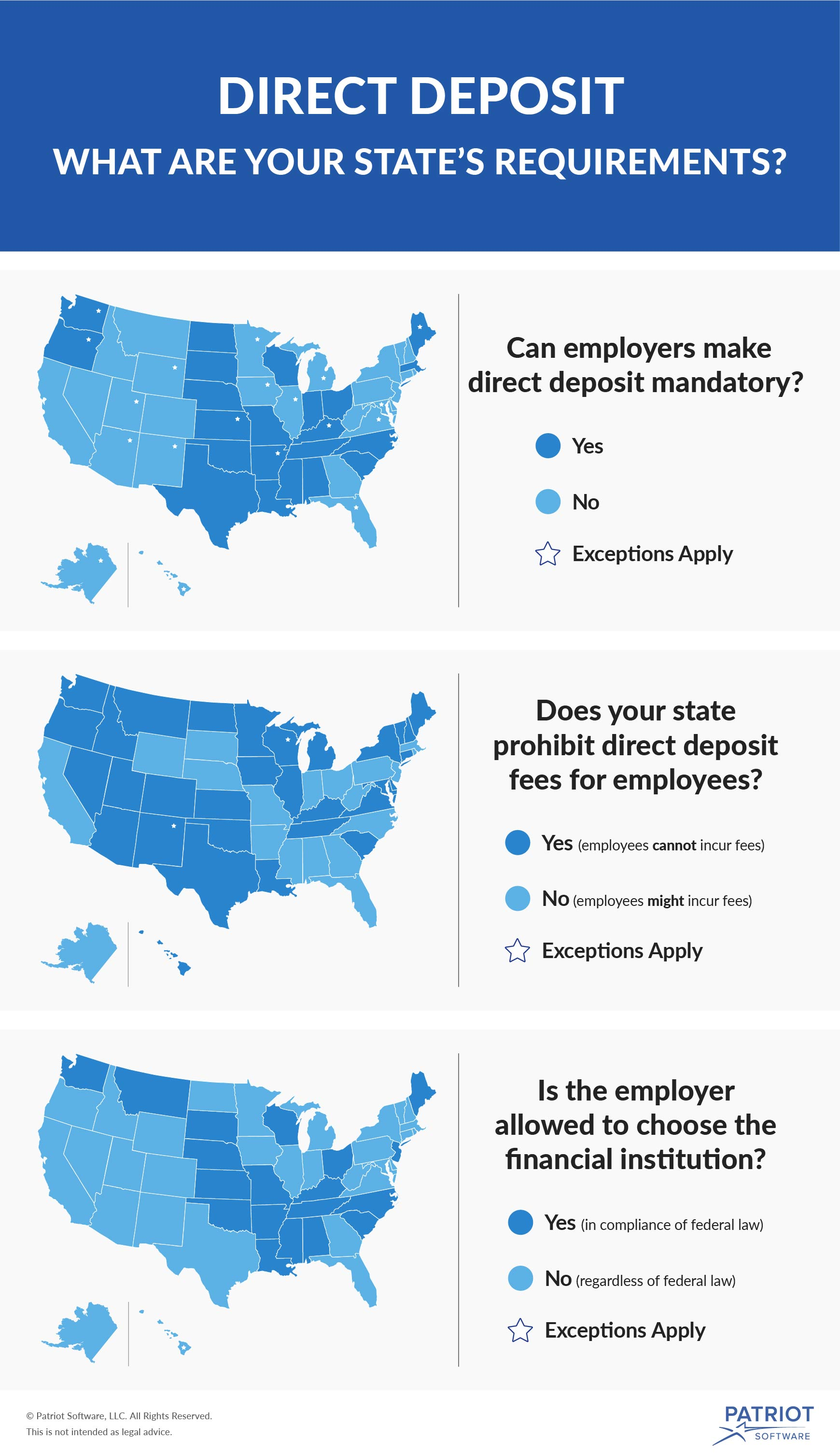

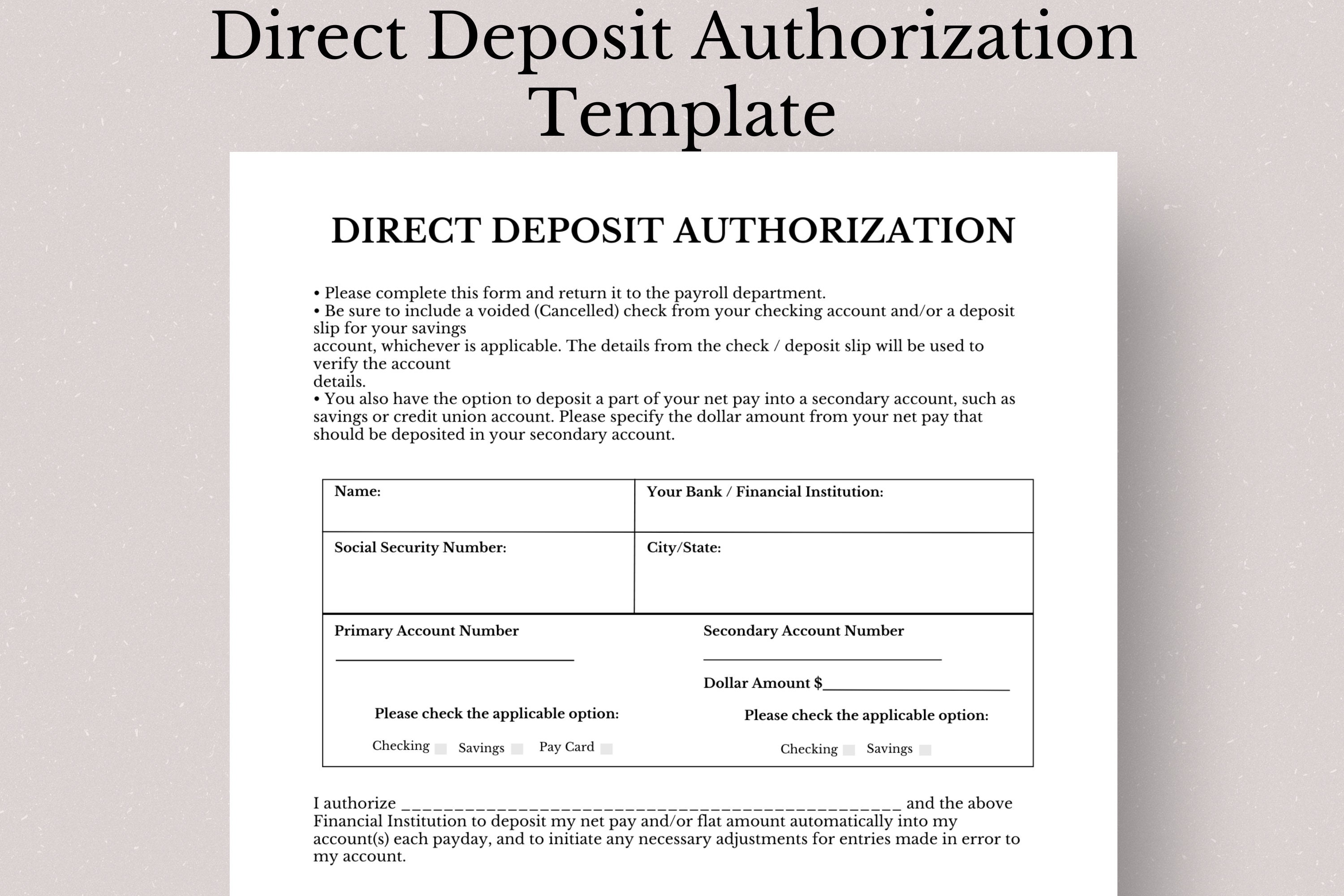

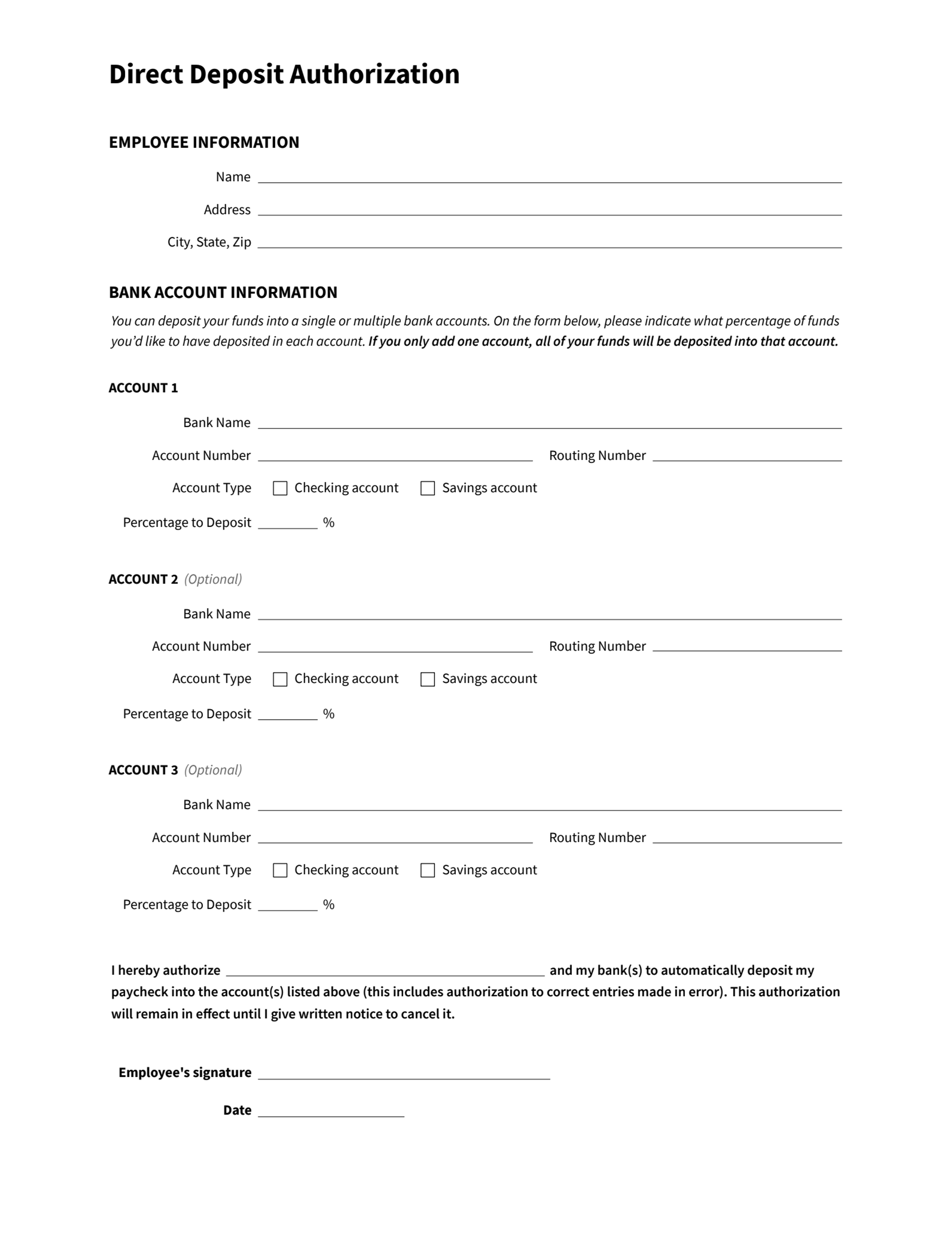

How does it work? The “Mandatory Direct Deposit Rule Every Employee Silently Follows” means employers are legally obligated in the U.S. to automatically deposit most qualifying wages into a designated bank account—provided the employee provides a confirmed bank routing and account number. No explicit announcement is needed; the system operates procedurally, enforced by payroll processors and banking compliance protocols. This setup protects employees from late payments while balancing employee choice with institutional responsibility, fostering trust in routine earnings processing.

Still, confusion lingers. Mandatory Direct Deposit: The Hidden Law Organizing Every Payday Common questions include: Does this apply to freelancers? Can employers bypass it? What happens if accounts change? In response, the rule primarily governs traditional W-2 employees and is tied to bank account verification—no blanket overrides by employers. Changes require formal employee update, and lapses are rare but possible. For gig workers in the gig economy, direct deposit remains optional but increasingly adopted as platforms integrate payroll tools.

While some assume it’s a recent mandate, it evolved from decades of financial infrastructure modernization—driven by consumer demand for reliability and employers seeking efficiency. Though not widely labeled a “rule,” its presence is felt daily: no missed paydays, fewer errors, consistent access to earned income. This quiet consistency supports broader economic confidence, subtly yet powerfully shaping financial behaviors across the U.S.

To address real concerns, here’s what employees should know: update bank details promptly, verify deposit accuracy, and use online banking for quick fixes. Employers must maintain data privacy, update records in line with IRS reporting standards, and communicate clearly during transitions. Misconceptions about control or access are understandable—but transparency and proactive communication reduce friction. The goal remains simple: a stable, predictable income stream, delivered without delay.

This rule applies across diverse workstyles—full-time, part-time, contract, and freelance—though usage varies. For salaried workers in traditional jobs, it ensures timely payments. For gig or independent professionals, adoption is growing as more platforms enable direct deposits to build financial credibility. Its silent role supports financial inclusion by normalizing reliable income flow, particularly among younger workers and those new to formal employment.

For readers navigating payroll changes or simply seeking clarity, awareness matters. The Mandatory Direct Deposit Rule Every Employee Silently Follows isn’t headline news, but understanding its function empowers smarter financial decisions. Staying informed prevents confusion, protects income timing, and builds trust in employment systems.

Stay informed not because it’s a headline, but because it’s a foundation—an everyday rule quietly shaping financial stability across the country. Knowing this rule enhances peace of mind and prepares you for income reliability in an evolving workplace.