The Fee That Doesn’t Matter—Until It Hurts Your Credit Score In a world where small financial choices ripple across credit histories, one overlooked charge continues to quietly shape scores: the surprise fee that rarely stops at “small.” “The Fee That Doesn’t Matter—Until It Ruins Your Credit Score” isn’t a warning flare—it’s a growing financial truth many users are realizing as late payments, default notices, or unnoticed account charges begin to influence their credit journey. In the U.S., where credit scores directly impact loan approvals, interest rates, and financial trust, paying attention to even seemingly trivial fees is no longer optional. Recent data shows rising user awareness around hidden charges, especially among millennials and Gen Z navigating credit for first homes, major purchases, or career mobility. How A 3-Day Late Fee Can Cost Your Savings×Fact Or Fiction? This article unpacks why this “small” fee deserves serious attention—not to incite fear, but to inform mindful financial habits.

Why The Fee That Doesn’t Matter—Until It Ruins Your Credit Score Is Gaining Attention in the US Recent economic shifts and digitized banking have amplified consumer exposure to diverse, often opaque fees. As financial products multiply and subscription models evolve, a quiet yet persistent fee—once dismissed as negligible—now surfaces repeatedly across finance forums, newsletters, and social conversations. What was once considered a minor cost, like a small late payment processor charge or a minor account monitoring fee, increasingly disrupts newly launched credit profiles or derails attempts to build strong scoring behavior. With credit scoring increasingly sensitive to payment timeliness and account activity, even brief financial friction can leave lasting marks. How A 3-Day Late Fee Can Cost Your Savings×Fact Or Fiction? This growing visibility reflects a broader public shift: users are no longer satisfied with surface-level fees—they seek context, pattern recognition, and proactive avoidance strategies.

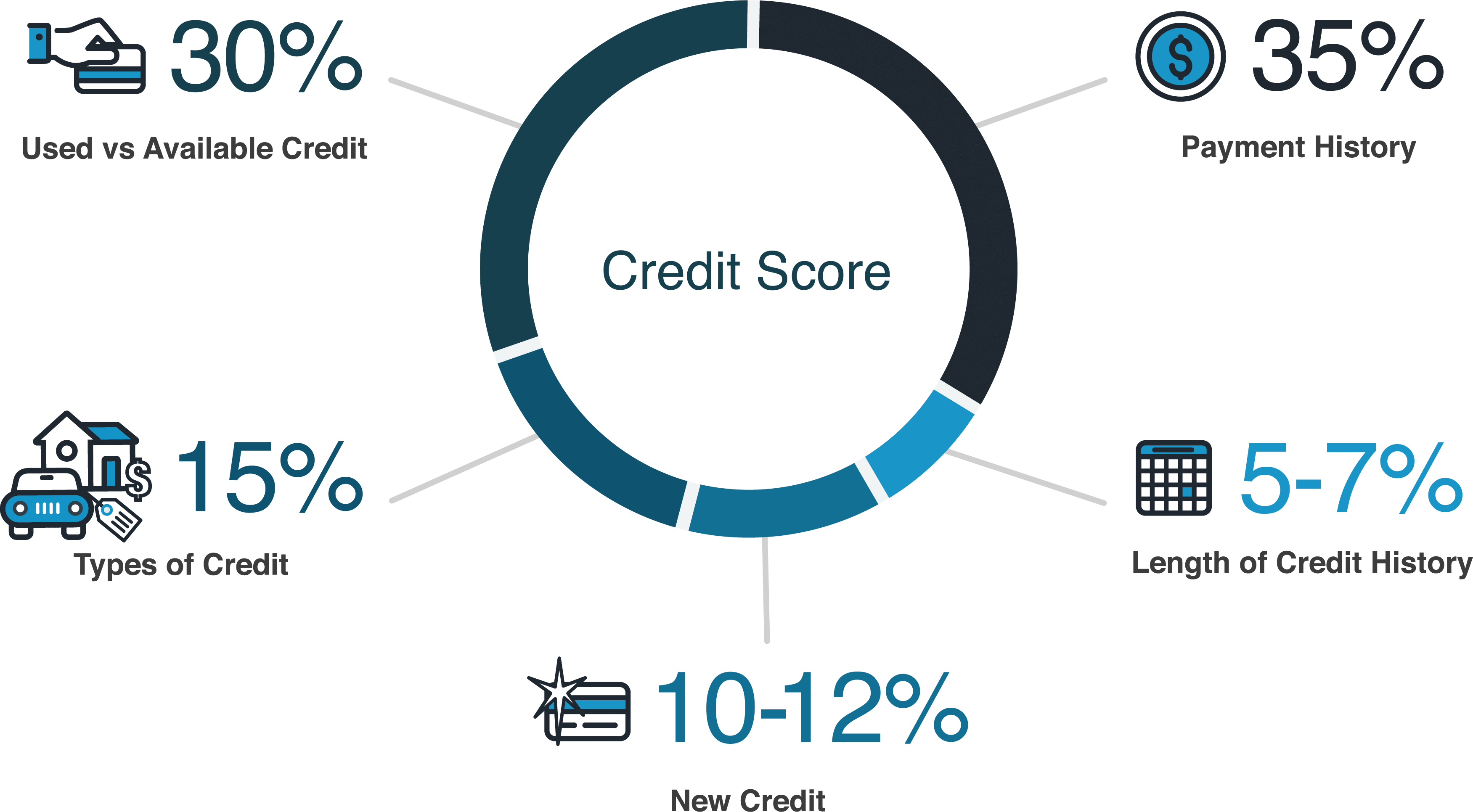

How The Fee That Doesn’t Matter—Until It Ruins Your Credit Score Actually Works The phenomenon occurs not through shock value alone, but through cumulative impact. A single unexplained $25 fee might seem inconsequential—but over months or years, such charges reduce payment history diversity, delay dispute resolution, and weaken creditworthiness signals. Credit bureaus analyze payment timeliness and account behavior over time, and recurring minor charges appear in reports as indicators of inconsistent financial management. Even automated systems flag clustering of small delinquencies as risk factors. How A 3-Day Late Fee Can Cost Your Savings×Fact Or Fiction? This fee often goes unrecognized initially because it appears in early transaction history or monthly statements with minimal wording. But over time, it compounds—manufacturing perceived instability that affects approval odds, lending terms, or rental applications. The real danger lies in cumulative effect, not isolated cost.

Common Questions About The Fee That Doesn’t Matter—Until It Ruins Your Credit Score

Q: Is any small fee actually harmful to credit scores? Not all fees damage credit instantly, but those that appear frequently, go unaddressed, or linger long-term erode payment history integrity. What matters is consistency and visibility—even small charges matter when they disrupt on-time payment records or show up repeatedly.

Q: Can a single $10 charge ruin my credit? While one fee rarely destroys a score, inconsistent small charges over months can weaken scoring patterns. Multiple minor delinquencies grouped closely in time signal instability, reducing scoring confidence.

Q: How often do people overlook these fees? Studies show nearly half of consumers admit to missing at least one late payment or small charge due to statement fatigue, digital clutter, or automatic payment defaults. This creates opportunity for overlooked fees to go unnoticed and unchallenged.

Opportunities and Considerations The key takeaway is awareness, not alarm. The fee that doesn’t matter turns meaningful when tracked proactively. Users gaining visibility into these charges develop sharper financial discipline—avoiding future surprises, improving payment consistency, and strengthening long-term credit positioning. On the flip side, ignoring or dismissing even minor fees entrenches risk. This fee isn’t a death knell—it’s a signal to build habits: reviewing statements weekly, confirming charges instantly, and setting up alerts for unusual activity. For those just beginning credit management, understanding its role is a critical first step toward financial resilience.

Who The Fee That Doesn’t Matter—Until It Ruins Your Credit Score May Be Relevant For This insight applies broadly: young professionals starting careers, first-time homebuyers securing mortgages, freelancers managing irregular income, and anyone rebuilding financial credibility after past setbacks. Even long-term homeowners can be affected by overlooked late fees or account fees impacting new credit lines. The fee’s significance grows with financial activity—especially when combined with interest or payment defaults. For anyone shaping a credit profile for the first time or reestablishing trust after a lapse, recognizing this risk is empowering.

Things People Often Misunderstand A common myth is that “small fees” rarely show up on credit reports. In reality, credit scoring providers track payment accuracy and account behavior closely—even minor charges contribute to payment history depth and timeliness. Another misconception is dismissing one-time fees as irrelevant, ignoring their aggregating effect. Trusted information sources clarify that all charges matter in context, especially when stacked over time. Building credit means not only paying bills on time but actively monitoring every fee, alerting to discrepancies, and asserting your financial responsibility when needed.

Soft CTA If navigating credit feels overwhelming, take a moment to review your monthly statements—just five minutes can reveal hidden charges that quietly shape your score. Stay curious, stay informed, and let each payment, no matter how small, build a stronger foundation. Understanding the full picture helps turn hidden risks into manageable habits.

Conclusion The fee that doesn’t matter until it ruins your credit score isn’t a myth—it’s a quiet financial reality shaping decisions across the U.S. It reveals how modern credit systems reflect not just payment amounts, but consistent, visible behavior. By staying aware, reviewing regularly, and treating every charge with intention, users transform reactive alerts into proactive strength. In a world where financial clarity opens doors, recognizing what does matter—even when it seems minor—creates lasting confidence, credit health, and peace of mind. Stay informed. Stay in control.