Shocking Mandatory Deposit Policy Rule You Cannot Ignore

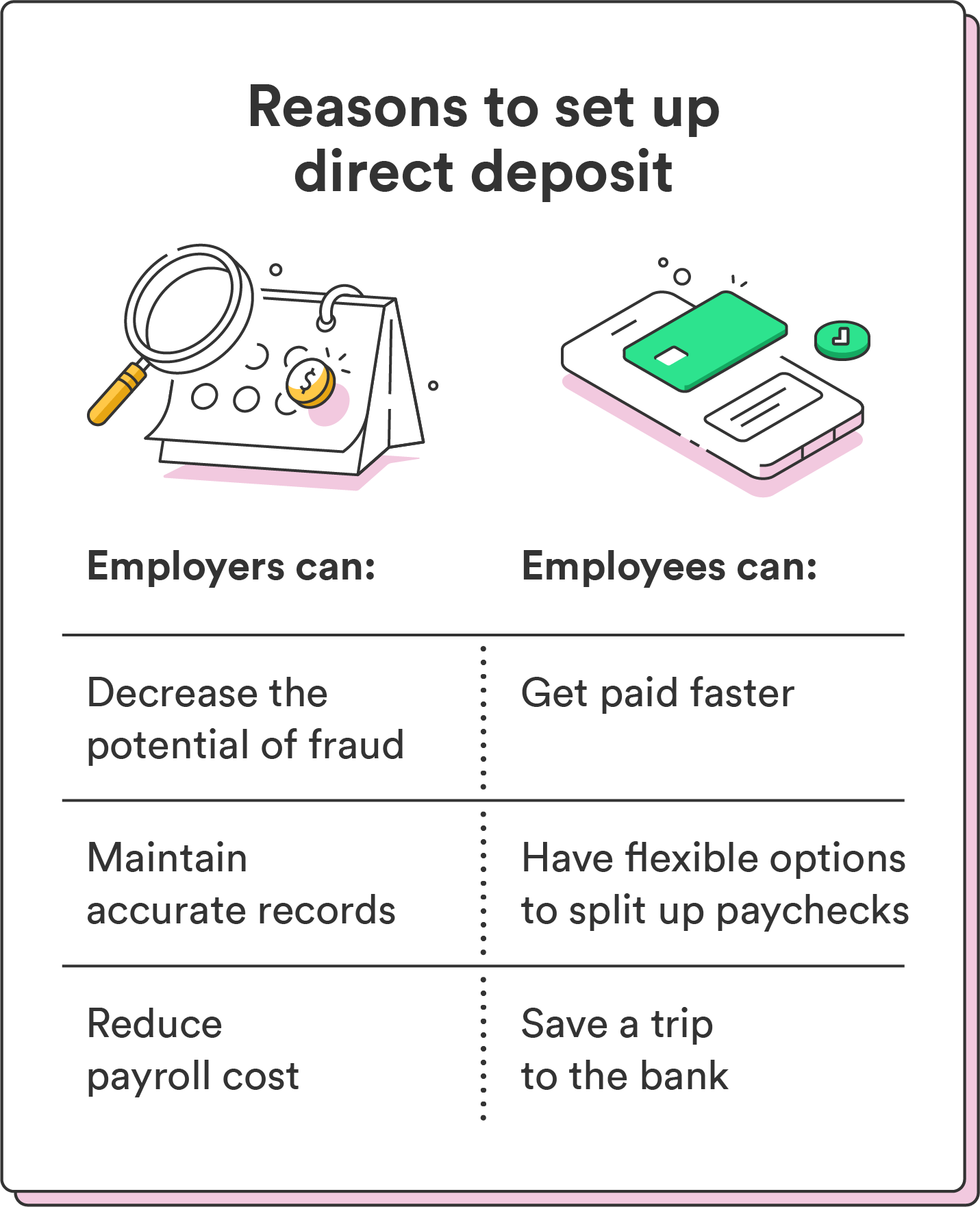

What’s rewiring real-time financial decisions across America? A new mandatory deposit policy rule reshaping digital transactions—one that’s already triggering widespread attention. Used to protect user accounts and stabilize platform integrity, this policy now sits at the intersection of consumer protection, compliance, and platform accountability. 5 Critical Reasons Mandatory Direct Deposit Now Protect Your Paycheck While not widely understood, its growing influence makes it a critical trend for anyone navigating modern financial systems.

Why Shocking Mandatory Deposit Policy Rule You Cannot Ignore Is Gaining Attention in the US

Digital transaction volumes in the US have skyrocketed, fueling demand for stronger safeguards against fraud and misuse. Recent regulatory shifts reflect a national push to standardize deposit controls across fintech, peer-to-peer platforms, and banking services. What’s emerging is a mandatory requirement: users must maintain minimum deposits before accessing certain transaction tiers. 5 Critical Reasons Mandatory Direct Deposit Now Protect Your Paycheck This rule, though designed for security, is sparking widespread discussion due to its tangible impact on everyday financial behavior and platform trust.

Despite being framed as a compliance measure, its ripple effects are shaping user habits, platform design, and trust in digital finance—making it impossible to overlook.

How Shocking Mandatory Deposit Policy Rule You Cannot Ignore Actually Works

This policy requires verified users to maintain a baseline deposit amount before executing high-value or rapid transactions. Unlike optional balance thresholds, it acts as a real-time gatekeeper. When a user initiates a transfer or exchange that exceeds the defined limit, a mandatory deposit is triggered—either automatically or via confirmation. 5 Critical Reasons Mandatory Direct Deposit Now Protect Your Paycheck This prevents impulsive actions, reduces fraud exposure, and ensures account stability before large movements occur.

The mechanism combines automated risk assessments with user authentication layers, minimizing friction while raising accountability. The result? A system that balances accessibility with safeguarding financial integrity.

Common Questions People Have About Shocking Mand deposit Policy Rule You Cannot Ignore

Q: Why do deposit mandates suddenly matter more? A: Increased cybersecurity threats and cross-border transaction volumes have prompted regulators to enforce stronger pre-transaction verification. This policy standardizes accountability across platforms and protects both users and providers.

Q: Does this affect every transaction? A: Not all. This 7-Step Direct Deposit Mandate Changes How You Receive Every Paycheck It applies only to transactions above a platform-specific threshold, designed to shield high-risk or high-value activity while preserving routine spending.

Q: How does it impact my bank account or app experience? A: Minor adjustments include brief deposit windows or small pre-authorizations, rarely disrupting everyday use. Why Your Paycheck Hangs On This Mandatory Direct Deposit Policy Transparent communication helps ease adaptation.

Q: Can I appeal or adjust my deposit requirement? A: Most platforms offer clear paths to review or reduce thresholds based on verified account activity and responsible usage history.

Opportunities and Considerations

On the upside, this policy strengthens trust in digital platforms, reduces fraud-related losses, and encourages disciplined financial behavior. For businesses, it presents a chance to innovate around transparent compliance tools and user education. On the downside, users accustomed to frictionless transfers may face brief delays, requiring adaptive interfaces and clear guidance. The key is balance—enforcing security without compromising accessibility.

Things People Often Misunderstand

A common myth is that the rule mandates permanent high deposits. In fact, it’s dynamic, context-sensitive, and designed for risk management—not indebtedness. Another misunderstanding equates it to personal punishment; rather, it protects users from accidental overtransactions and platform exploitation. These nuances reflect careful policy design, not overreach—built to foster safer, informed financial ecosystems.

Who Shocking Mandatory Deposit Policy Rule You Cannot Ignore May Be Relevant For

This rule applies across multiple user segments. For solo entrepreneurs managing freelance funds, it ensures transaction legitimacy and financial accountability. For family users coordinating shared accounts or digital wallets, it introduces structured deposit controls that simplify shared liability. Platform operators in fintech, payment processing, and digital banking must also adapt systems to compliance without alienating users. Even those exploring decentralized finance or crypto platforms are increasingly encountering similar verification layers—making awareness essential.

Soft CTA: Stay Informed and Empowered

Understanding the Shocking Mandatory Deposit Policy Rule You Cannot Ignore is more than legal compliance—it’s part of smarter, safer digital engagement. Platforms are evolving, and staying ahead means embracing transparency, not fear. Stay informed through trusted financial news sources and explore how these policies shape the future of money in America—without pressure, just clarity.

![50 Effective Security Deposit Return Letters [MS Word] ᐅ TemplateLab](https://templatelab.com/wp-content/uploads/2019/03/security-deposit-return-letter-07.jpg)