NEVER Assume: Renters Insurance Doesn’t Cover Earthquakes — Reality Is Scary

When renting a home, most people assume their insurance protects everything — furniture, electronics, walls, even personal loss. But the truth about earthquakes hits differently. Start Now: How To Break Laser-Trained Aggression In Las Vegas Dogs A staggering gap exists: renters coverage rarely if ever includes earthquake damage. For too many, this silence creates danger. In cities across the U.S., from California’s fault lines to the midwest’s hidden risks, awareness is rising — not from fear, but from clear-eyed understanding.

Why NEVER Assume: Renters Insurance Doesn’t Cover Earthquakes — Reality Is Scary Is Gaining Attention in the US

Recent natural events and rising costs have turned a quiet risk into a widely discussed reality. Start Now: How To Break Laser-Trained Aggression In Las Vegas Dogs Renters across the country are asking: “Do I need extra coverage if my renters policy doesn’t include earthquakes?” The answer isn’t just technical — it’s personal. With climate-driven seismic threats increasing and repair costs soaring, ignoring this gap is a gamble no tenant can afford. Despite the hesitation, data shows rising concern: surveys now show nearly one in three renters haven’t checked their policy details — a wake-up call in a market where preparedness means safety.

How NEVER Assume: Renters Insurance Doesn’t Cover Earthquakes — Really Works That Risk

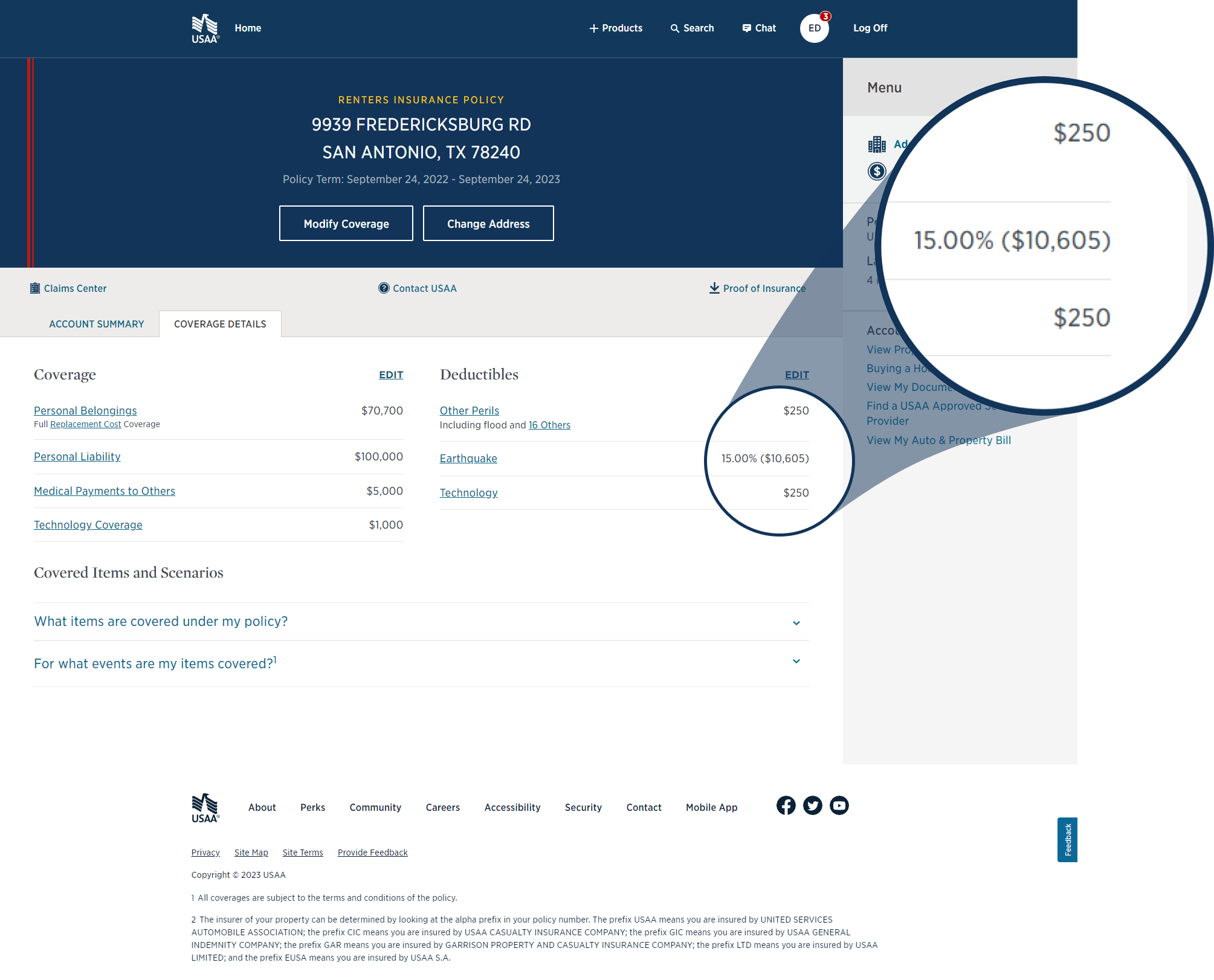

Most renter’s insurance policies explicitly exclude earthquake damage, citing its low probability but high cost. Start Now: How To Break Laser-Trained Aggression In Las Vegas Dogs Unlike fire or theft, earthquakes strike suddenly and impact entire neighborhoods. Without coverage, replacement of vital valuables or structural repairs can cost tens of thousands of dollars — often well beyond standard deductibles. This exclusion isn’t a loophole; it’s a widely recognized underwriting standard. But the assumption that “it won’t happen here” persists — even as seismic data paints a broader picture of risk across multiple states.

Common Questions People Have

H3: Do I need earthquake coverage if my landlord’s insurance includes structural damage? No. Landlord policies typically cover building structure but exclude contents and often overlook earthquake perils. A fire or burst pipe claim is covered, but sudden seismic shaking causing collapse or equipment failure usually isn’t.

H3: What if I file a claim after an earthquake — can I recover anything? Insurance companies rarely pay for earthquake damage under renters policies. Claims are denied or limited unless you’ve purchased an add-on earthquake rider. Documentation and proof of exposure still matter, but coverage is highly conditional.

H3: What’s the cost of adding earthquake coverage? Premiums vary but typically add $25–$60 monthly. Given average repair costs, this is small protection against catastrophic loss — especially in medium- to high-risk zones. Here's What Really Protects You: Does Your Renters Policy Cover Seismic Risks?

Opportunities and Considerations

Adding earthquake coverage offers critical peace of mind without overpaying. Premiums remain low compared to potential losses, and policies often include rapid assessment tools post-event. Still, renters should evaluate location risk — proximity to faults, building age, soil type — and review policy details carefully. Not every area faces equal threat; real estate and insurance data help tailor decisions. The key is informed awareness — not panic.

Things People Often Misunderstand

Many assume earthquakes are rare or only hit “California-style zones,” but modern seismic maps show active fault lines across the U.S., including the Northeast and Midwest, with historically significant activity. Others believe homeowner policies automatically protect against all natural disasters. 7 Shocking Secrets To Stop Dog Aggression In Las Vegas Before It Starts The truth: renter’s coverage focuses on common risks, not rare extreme events. Without explicit inclusion, earthquakes fall through the cracks — a gap more common than public understanding.

Who NEVER Assume: Renters Insurance Doesn’t Cover Earthquakes — Reality Is Scary May Be Relevant For

This applies whether you rent in a high-risk city like Seattle or a lower-risk area with aging infrastructure. Families with young children, homeowners with costly goods, and business renters handling inventory all face unique stakes. Even short-term renters benefit — a single event can turn weeks into months of disruption. The risk isn’t theoretical: past claims show losses exceeding $100,000 per household in major quakes.

Soft CTA: Stay Informed, Not Scared

Knowledge is power. Check your policy details. Inquire about add-ons. Use resources like FEMA and state geological surveys to assess local risk. Preparedness isn’t about fear — it’s about protecting what matters, without unnecessary expense. Small steps can make a big difference when disaster hits.

Conclusion

Earthquake risk is real, widespread, and often misunderstood — not just for renters in high-risk zones, but across much of the country. “NEVER Assume: Renters Insurance Doesn’t Cover Earthquakes — Reality Is Scary” reflects a growing truth: coverage gaps are not rare, and ignoring them has real cost. By staying informed, reviewing policies, and considering add-ons when needed, renters can turn uncertainty into confidence. Safety starts not with panic, but with clarity — and that begins right now.

_01042023182956935.png)