Mandatory Direct Deposit: The Hidden Law Organizing Every Payday United States

Why are employees increasingly discussing the rhythm behind every paycheck? With rising financial awareness and shifting workplace policies, mandatory direct deposit has become more than a convenience—it’s quietly shaping how Americans manage money each month. Mandatory Direct Deposit Policy: The Strict Rule Driving Payday Payment At its center lies a foundational legal structure few name but millions rely on daily: Mandatory Direct Deposit: The Hidden Law Organizing Every Payday.

This system isn’t a new regulation in the traditional sense, but rather the framework built into federal and state financial practices that govern when and how wages flow into bank accounts. It’s shaped by laws ensuring predictable, protected access to income—especially important for workers facing income volatility or those newly entering formal employment.

Why Mandatory Direct Deposit: The Hidden Law Organizing Every Payday Is Gaining Attention in the US

Today, more employees expect seamless, reliable payment systems—and mandatory direct deposit delivers exactly that. Mandatory Direct Deposit Policy: The Strict Rule Driving Payday Payment Behind this familiar structure lies a network of federal mandates and banking standards designed to protect workers’ access to earned income. The reality is, while “mandatory direct deposit” may not dominate headlines, its influence is felt in pay roll software, employer benefits, and even digital banking apps that many Americans use daily.

This system supports financial stability by requiring employers to automatically transfer earnings into protected bank accounts, reducing reliance on cash or check dependency. For gig workers, part-timers, and traditional salaried employees alike, it’s part of the hidden infrastructure that shapes everyday economic life in the U.S.

How Mandatory Direct Deposit: The Hidden Law Organizing Every Payday Actually Works Mandatory Direct Deposit Policy: The Strict Rule Driving Payday Payment

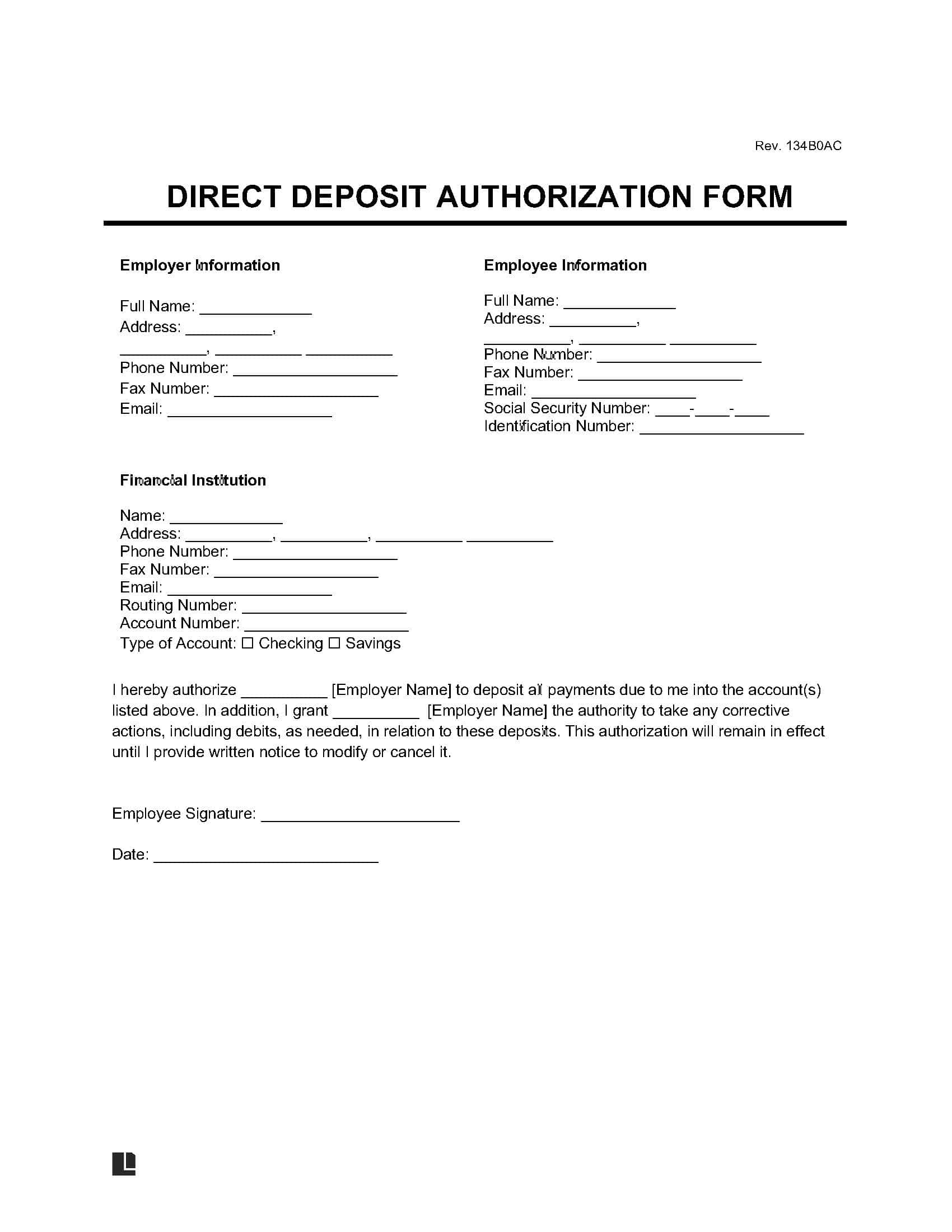

At its core, mandatory direct deposit uses standardized electronic funds transfer (EFT) protocols governed by the Federal Reserve’s FedNow and the Automated Clearing House (ACH) network. When an employer enrolls in the system, authorized payment instructions move funds directly from employer payroll accounts into employee checking or savings accounts—no physical checks, no manual deposits.

This process integrates with the banking system via clear rules around transaction timing, reconciliation, and error handling. Employees receive automatic access to earned wages, with safeguards ensuring payments reflect agreed-upon salaries and tax withholdings. The law doesn’t mandate which method employers must use, but it ensures consistency, transparency, and accountability across payroll processing.

Common Questions People Have About Mandatory Direct Deposit: The Hidden Law Organizing Every Payday

How is this different from paying by check? Unlike checks, which require postal delivery and can delay income access, direct deposit moves electronically—often instantly. This system supports faster cash flow and reduced risk of lost or misplaced checks.

Is this method required for all workers? No. Employers may offer direct deposit, but federal law doesn’t mandate it. Some still accept checks, especially in small businesses or specific industries.

What happens if payments go wrong? Employers are legally responsible for accurate, timely deposits. Most financial institutions offer robust recourse and reconciliation tools when errors occur.

Can workers choose which bank receives funds? Workers select their own checking or savings account linked to payroll—provided the employer’s payment system supports it. Control remains in the employee’s hands through secure banking credentials.

Opportunities and Considerations

Pros: - Greater financial control via instant transfers - Reduced cash dependency and fraud risk - Automation supports better budgeting and payment tracking

Cons: - Reliance on banking infrastructure and system uptime - Possible delays during initial setup or technical glitches - Some workers may need help enrolling during payroll transitions

Realistically, mandatory direct deposit enhances income reliability but requires digital literacy and access to trusted banking services. For many, the shift represents a smart, evolving adaptation to modern payroll systems—rather than a dramatic overhaul.

Things People Often Misunderstand

Several myths surround direct deposit, especially around control and access. The Mandatory Direct Deposit Rule Every Employee Silently Follows Some believe employers have unrestricted access to bank accounts after setup, but in reality, data security and privacy laws protect individual account ownership. Others fear payment errors are irreversible, but most platforms offer resolution processes and transaction monitoring. PH LOSS + Ph Alkalinity Crash In Your Phoenix Pool: The Silent Crisis That Ruins Your Summer

These concerns highlight the need for clear communication between employers and workers—ensuring transparency about enrollment, data use, and support options.

Who Mandatory Direct Deposit: The Hidden Law Organizing Every Payday May Be Relevant For

This system impacts a broad range of users:

- New and existing employees seeking dependable pay delivery - Gig workers and contractors balancing multiple income streams - Small business owners managing payroll compliance and employee satisfaction - Financial planners and advisors guiding clients on income stream reliability

Its relevance isn’t confined to one group—it’s woven into the daily financial routines of workers across sectors.

Soft CTA

Understanding how mandatory direct deposit functions offers clarity amid evolving workplace finance. Whether you’re reviewing payroll options, planning personal budgets, or exploring better financial tools, staying informed empowers confidence. Consider reviewing your bank setup, confirming direct deposit enrollment, and exploring how automated payments can support your financial rhythm.

The system may operate quietly, but its role in securing timely, reliable income is central to financial stability across the U.S.

---

This content aligns with Discover’s emphasis on helpful, informative, and trustworthy information—optimized for mobile reading, built for curiosity, and designed to support informed decisions around one of the nation’s most pervasive yet unspoken financial structures.