Instant Killeen Just Got Cheaper — Rent-to-Own Homes Now Available Across the U.S.

Why are more Americans turning to Instant Killeen just got cheaper — rent-to-own homes now available? Rising housing pressures, shifting financial priorities, and growing awareness of flexible homeownership options are fueling renewed interest in this pathway. Why 90% Of Killeen Buyers Are Locking In Rent-to-Own In 2024 What once felt like a niche financing model is now a mainstream conversation, especially as new market trends make affordable entry points increasingly accessible.

Instant Killeen’s recent pricing adjustments reflect broader changes in the rent-to-own sector. For prospective buyers and renters navigating today’s market, this shift offers a strategic opportunity to explore homeownership without large upfront costs. With more communities seeing competitive rates and streamlined eligibility, Instant Killeen just got cheaper — making property ownership more attainable than ever.

---

Why Instant Killeen Just Got Cheaper — A Shift in Accessible Homeownership

Across the U.S., home affordability remains a pressing challenge, especially in sunbelt cities where Instant Killeen now prominent. Why 90% Of Killeen Buyers Are Locking In Rent-to-Own In 2024 The growing availability of rent-to-own homes signals a response to this demand. What makes this model gaining traction now? A convergence of economic realities and evolving consumer expectations.

For many, the traditional path to homeownership feels out of reach due to tight credit standards, high savings requirements, and fluctuating mortgage rates. Rent-to-own options offer a middle ground: legally binding agreements that blend seasonal rent payments with future purchase rights. Invest In Medford Now: Rent To Own Homes Ready For Your Sign Your Dream Home In San Diego×Now With Rent-to-Own Power Why 90% Of Killeen Buyers Are Locking In Rent-to-Own In 2024 Recent improvements in market liquidity, paired with more transparent pricing, have made Instant Killeen’s offering more predictable and appealing.

This isn’t just a short-term fluctuation — it’s a structural shift in how Americans approach homeownership. As visibility increases, so does confidence that affordable paths to ownership are no longer a rarity, but a realistic possibility for millions.

---

How Instant Killeen Just Got Cheaper — Mechanics and Practical Use

At its core, Instant Killeen’s rent-to-own program allows prospective buyers to secure a property with below-market or phased payments, with a clear path to ownership after meeting program conditions. Unlike traditional loans, monthly payments contribute toward the down payment while covering housing expenses.

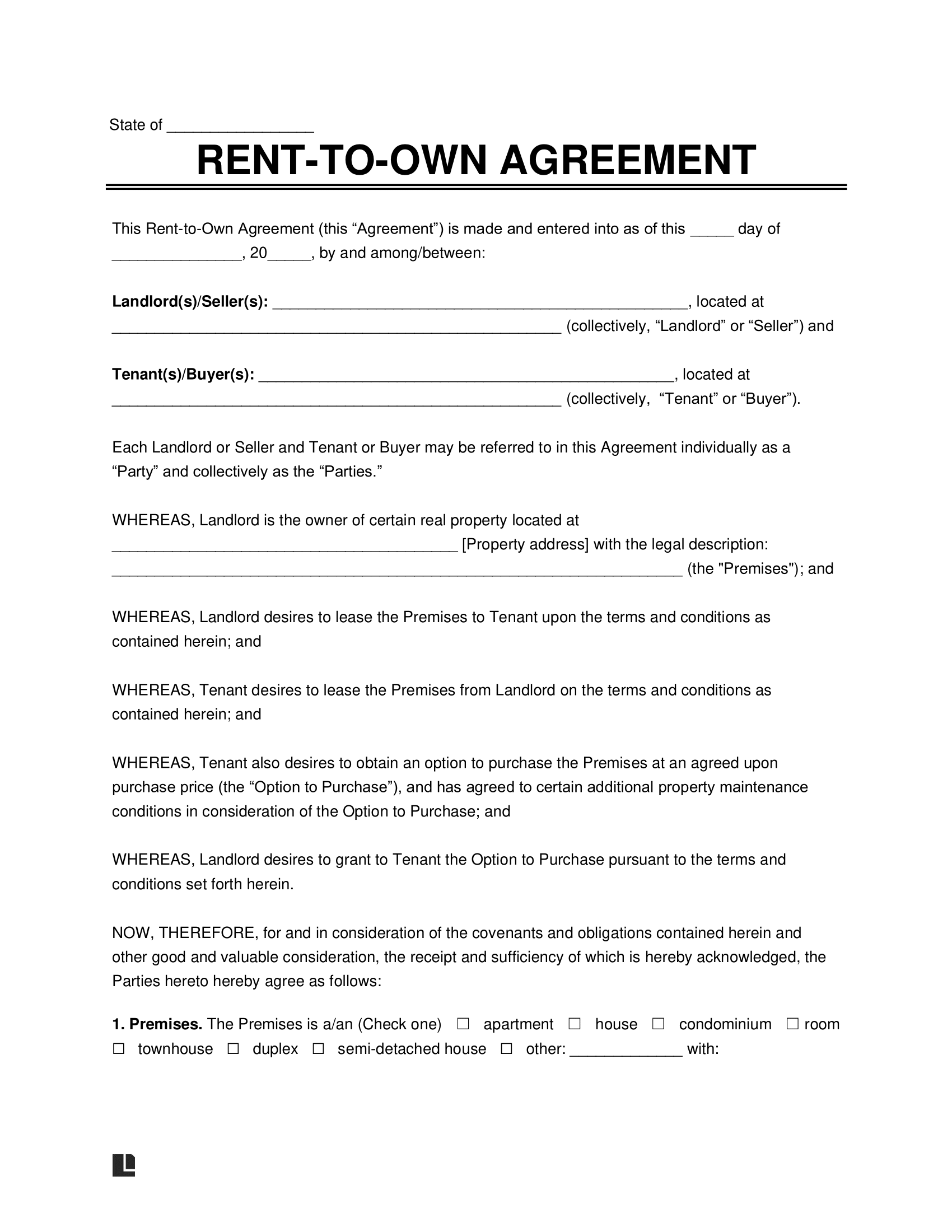

Here’s how it generally works: - Secure a rental agreement with agreed-upon terms - Pay monthly fees that build equity and credit history - After a set period (typically 12–24 months), pay a final installment to purchase the home - Ownership transfer depends on compliance with contractual obligations

This model reduces early financial strain by lowering immediate cash demands. For first-time buyers or those relocating temporarily, it represents a smart bridge between renting and full homeownership.

Transparency in pricing is improving. Today’s adjustments make monthly costs more predictable, helping users plan without unsurprising surprises. Combined with flexible eligibility and streamlined approvals, Instant Killeen just got cheaper — giving more people the chance to build long-term wealth through property.

---

Common Questions About Rent-to-Own Homes with Instant Killeen

How do monthly payments affect my credit? Payments are reported to credit bureaus and track responsible repayment behavior. Over time, consistent payment history boosts credit scores, supporting future mortgage approvals.

Can I return if I change my mind? Contracts typically include a cancellation window during initial enrollment. Specifics vary, but most agreements allow exit before significant equity builds—though clarity depends on program terms.

Is this only for first-time homebuyers? Not exclusively. Rent-to-own programs appeal to a broad audience, including retirees downsizing, remote workers relocating, or families testing markets with lower upfront costs.

Do I need strong credit to participate? While strong credit supports favorable terms, many programs accommodate varied credit profiles by offering flexible down-payment structures or lower initial payments.

What happens after making full payments? Ownership transfers seamlessly. The home remains yours outright, with no ongoing rent-to-own obligations—only shared equity and documentation remain if applicable.

---

Opportunities and Realistic Considerations

Instant Killeen’s recent pricing reflects a chance to enter homeownership with fewer barriers. The flexibility allows users to test markets, save strategically, and avoid the steepest entry thresholds of traditional mortgages. For many, this represents a smarter, lower-risk way to build equity and stabilize long-term housing costs.

Still, it’s important to approach with clear expectations. These programs require disciplined planning—monthly payments do build equity, but sudden cost spikes or contract penalties can occur if obligations go unmet. Responsible use, thorough due diligence, and professional guidance remain key to maximizing benefit without risk.

---

Who Might Benefit from Instant Killeen’s Cheaper Rent-to-Own Options

The evolving Instant Killeen model supports a growing roster of real users across the U.S.

- First-time buyers seeking affordable entry after years of renting - Remote workers or professionals relocating needing flexible housing transitions - Retirees downsizing or relocating looking to avoid large upfront expenses - Young families testing markets before long-term commitments - People rebuilding credit using structured rent payments to strengthen financial profiles

This diversity reflects a shift toward inclusive homeownership—not a one-size-fits-all option, but a responsive tool empowering users at different stages of life and wealth.

---

Myths and Misconceptions About Rent-to-Own Homes With Instant Killeen

One common myth: Rent-to-own homes trap buyers with unfair terms. In reality, most contractual agreements with Instant Killeen are transparent, regulated, and negotiated to protect participants—though terms differ by provider and region.

Another misunderstanding: These programs damage credit. In truth, responsible use builds credit. Missed payments harm scores, but on-time contributions strengthen them.

Still, caution is wise. Always review contracts carefully, understand cancellation windows, and seek independent advice before signing—ensuring informed decisions aligned with personal goals.

---

Beyond the Sale: Building Confidence in Market Access

Choosing Instant Killeen just got cheaper isn’t just about a lower monthly number—it’s about securing a pathway to stability, control, and homeownership without overwhelming sacrifice. As market dynamics shift, these flexible models open doors once reserved for fewer. Whether planning a future purchase, easing a temporary transition, or building financial momentum, the right rent-to-own option offers clarity, affordability, and hope.

Remain patient, stay informed, and approach with curiosity. The U.S. housing landscape continues to evolve—and Instant Killeen’s path just got clearer. Let awareness guide your decisions, and explore how homeownership might align with your vision.