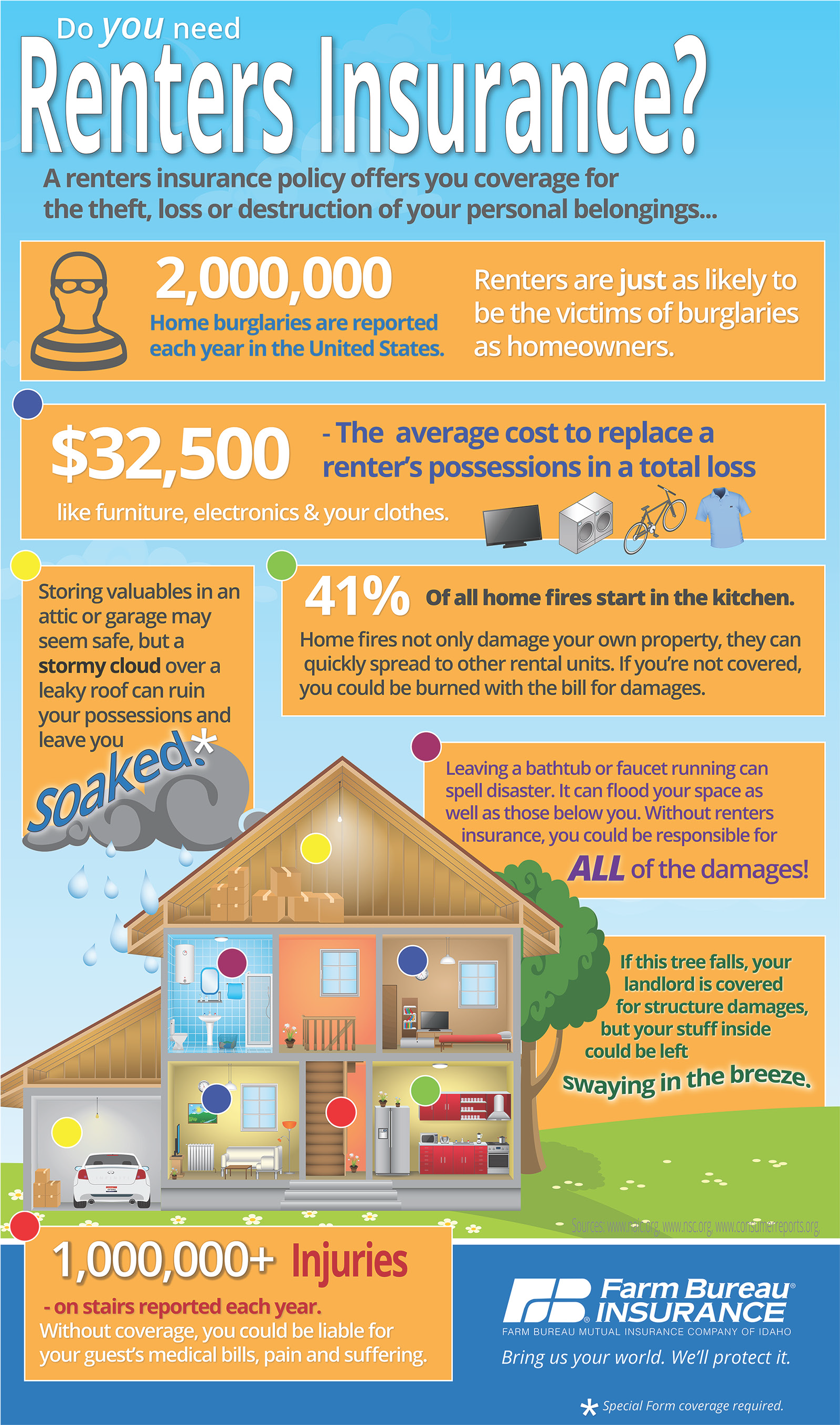

Hunting For Earthquake Coverage? Your Renters Insurance Is Cheating You

When the ground shifts beneath your feet—or even before it does—many Americans begin quietly questioning whether their renters insurance truly protects against nature’s unpredictability. This curiosity isn’t fringe—it’s widespread. Reports of rising property damage from seismic events, combined with rising insurance costs and gaps in standard coverage, have many asking: Hunting For Earthquake Coverage? 7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes Your Renters Insurance Is Cheating You. In a US market where natural disaster preparedness meets financial planning, understanding these gaps is more urgent than ever. With rising inflation and an increasing frequency of earth tremors in certain regions, the conversation around seismic risk is no longer niche—it’s mainstream. And while full earthquake insurance remains elusive for many renters, awareness of coverage options and their limitations is growing. This article reveals what you need to know about hunting earthquake coverage, why current renters policies often fall short, and how to think critically about protecting your home—and wallet. 7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes

Why Hunting For Earthquake Coverage? Your Renters Insurance Is Cheating You — Because the Gap in Protection Is Real

Renters insurance, as typically structured, rarely includes comprehensive earthquake coverage. While it protects against fires and theft, seismic events often fall outside standard policies. This disconnect drives frustration. 7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes Many users assume renters insurance is a failsafe during disasters—especially in high-risk zones—but the reality is far more nuanced. The Federal Emergency Management Agency estimates that over 50% of U.S. renters in earthquake-prone areas lack sufficient protection, leaving them vulnerable to catastrophic financial loss. Meanwhile, premiums for standalone earthquake policies remain high in many regions, creating a perceived affordability gap. What users often overlook is the hidden cost: repairs and rebuilding after seismic activity can easily exceed $100,000—far beyond coverage limits in basic renters plans. The search for alternatives isn’t reckless—it’s a rational response to incomplete protection.

How Hunting For Earthquake Coverage? Your Renters Insurance Is Cheating You — Works When You Understand the Nuances

Contrary to perception, “hunting” earthquake coverage isn’t about chasing conspiracy or scams—it’s about researching legally sound add-ons, supplemental policies, and regional programs designed to bridge gaps. Many renters find that layered protection—combining their existing policy with specialty endorsements or state-backed programs—offers better value than unproven market offerings. For instance, in California and Oregon, state-run initiatives supplement private coverage for earthquake risks, reducing premiums and expanding coverage breadth. Even when full standalone coverage isn’t feasible, proactive research enables smarter decisions. Users who dig into policy exclusions, deductible structures, and endorsement availability often discover affordable ways to secure meaningful protection without overspending. The key is awareness: hunting here means informed exploration, not hype.

Common Questions About Hunting For Earthquake Coverage? Your Renters Insurance Is Cheating You

Q: Does renters insurance cover earthquakes? A: No, standard renters insurance typically excludes earthquake damage. Renters policies focus on personal property loss from fires, theft, or vandalism—not seismic events.

Q: Can I add earthquake coverage to my current renters policy? A: Rarely “additionally.” Most insurers don’t allow endorsements; however, specialized insurers and state-backed programs in high-risk zones offer bundled or tailored earthquake riders and supplemental plans.

Q: How much does earthquake coverage cost? A: Premiums vary wildly by location—coastal and inland fault zones see higher rates. On average, a $100,000 replacement cost policy averages $200–$600 annually but can exceed $1,000 in high-risk areas.

Q: Is there government help for earthquake coverage? A: Yes. The National Earthquake Insurance Program (NEIP) offers federal incentives in some states, and FEMA support grants help with mitigation. Some rental communities also partner with risk pools to reduce costs.

Q: Can I qualify for lower rates without full coverage? A: Absolutely. Some insurers offer discounts for seismic retrofitting, premium payment plans, and claims history. Reducing deductibles or bundling with other coverages (e.g., flood) can lower costs significantly.

Opportunities and Considerations: Is Hunting For Earthquake Coverage Worth It?

Pursuing earthquake coverage as part of a broader preparedness strategy offers real value—but it demands realistic expectations. The upfront cost is undeniable, and coverage limits often require careful budgeting. However, the alternative—to face a major seismic event with minimal financial safety—carries far higher long-term risk, especially in aging rental markets where structural vulnerability compounds losses. Many renters underestimate cumulative impact: repair costs often exceed insurance limits, leading to decades of debt. For risk-aware users, especially coastal renters and urban renters in fault zones, hunting coverage isn’t a luxury—it’s essential risk management. Yet for others, incremental steps—documenting valuables, securing retrofitting advice, monitoring policy updates—may be more practical.

Misunderstandings to Avoid When Hunting For Earthquake Coverage? Your Renters Insurance Is Cheating You

A key myth: “Renters insurance covers everything—earthquakes included.” The truth is, renters policies exclude seismic damage by design. Another confusion: assuming government aid covers all costs. In reality, federal and local programs assist with mitigation and recovery but rarely fund full rebuilding. Some users also believe earthquake insurance is too expensive and unnecessary unless living in a fault zone—yet smaller tremors and liquefaction risks extend vulnerability far beyond major fault lines. Lastly, many think standalone policies offer one-size-fits-all protection; in truth, riders, endorsements, and bundled solutions tailor coverage precisely to risk profile and budget.

Who Might Hunting For Earthquake Coverage? Your Renters Insurance Is Cheating You — A Broad and Balanced Audience

This conversation spans renters from quake-prone states like California, Alaska, and Washington to renters in growing urban centers across the Midwest and Northeast where fault zones are less obvious but seismic risk is rising. First-time renters often search instinctively after exposure to disaster news. Shocked Renters × Earthquakes Aren't Covered, But You Paid For It Homeowners renting in fault zones actively seek protection. Even renters in low-risk areas increasingly ask: “For future resilience?” The question crosses income levels—from renters prioritizing stability to investors protecting property value. Urban professionals, remote workers, and families alike face a shared reality: natural disasters don’t respect geography. Thus, hunting informed, accessible coverage isn’t just for high-risk groups—it’s for anyone who values security in an unpredictable world.

A Soft CTA: Stay Informed, Not Alarmed

The truth is, there’s no single “hunting” strategy—only informed patience. Stay curious. Track evolving coverage options, policy updates, and local preparedness workshops. Use trusted tools to compare endorsements, assess risk, and understand your true exposure. When it comes to earthquake coverage, the best approach isn’t rushing into buy-or-don’t buy—but building awareness and readiness. Protect not just your belongings, but your peace of mind. This isn’t about fear—it’s about empowerment. In a world where preparedness shapes resilience, hunting for the right coverage today doesn’t just answer a question—it builds a safer tomorrow.