Earthquakes And Renters Insurance: The Dire Gap You Can’t Ignore Now

When a major quake rattles a major U.S. city, many pause to consider home protection—yet renters remain unusually blind to one critical protection: renters insurance covering earthquake damage. This invisible gap is widening at a time when seismic risk is growing, urban density is rising, and housing costs continue to climb. For tenants across the country, understanding the real limits of standard policies can mean the difference between recovery and long-term financial strain. NEWS: Renters Insurance Leaves Earthquake Damage Totally Uncovered × Here's Why

As climate-driven natural events surge and older urban infrastructure ages, experts are sounding a quiet wake-up call: renters insurance rarely covers earthquake damage, leaving many unprepared when the ground shifts beneath their feet. This growing mismatch between real world risks and policy coverage is no longer a niche concern—it’s a national conversation gaining momentum.

Why Earthquakes And Renters Insurance: The Dire Gap You Can’t Ignore Now Is Gaining Attention in the US

Across the U.S., seismic activity is increasing—especially along the West Coast, but also in hidden fault zones in the Midwest and Southeast. Recent events, combined with mounting data on aging building materials and dense urban housing, highlight an escalating exposure for renters who assume their standard tenant insurance offers full protection. NEWS: Renters Insurance Leaves Earthquake Damage Totally Uncovered × Here's Why In reality, most policies exclude earthquake damage, focusing only on fire, theft, or liability—leaving renters exposed to high repair costs, disrupted living, and long-term financial vulnerability.

Current trends show growing awareness among renters, urban planners, and insurers. As housing costs strain budgets and tenant advocacy gains traction, questions about seismic preparedness are rising faster than ever. The silence around earthquake risk in renters coverage hasn’t lasted long—curiosity, concern, and demand for clearer answers are driving this national conversation forward.

How Earthquakes And Renters Insurance: The Dire Gap You Can’t Ignore Now Actually Works NEWS: Renters Insurance Leaves Earthquake Damage Totally Uncovered × Here's Why

Earthquakes strike without warning and can cause widespread structural damage—even in modern buildings. Renters insurance typically covers personal belongings and liability but explicitly excludes damage from ground shaking, soil liquefaction, or falling debris. This is by design: insurance underwriting follows rigorous risk modeling, and earthquakes fall into a high-consequence, low-frequency category that insurers adjust for through policy exclusions.

However, this exclusion is not about coverage failure—it’s about managing risk at scale. Renters insurance serves its purpose for common hazards, but seismic events demand specialized planning. The gap exists because most renters assume their standard policy provides comprehensive protection. Understanding what’s missing is the first step toward closing the divide.

Common Questions People Have About Earthquakes And Renters Insurance: The Dire Gap You Can’t Ignore Now

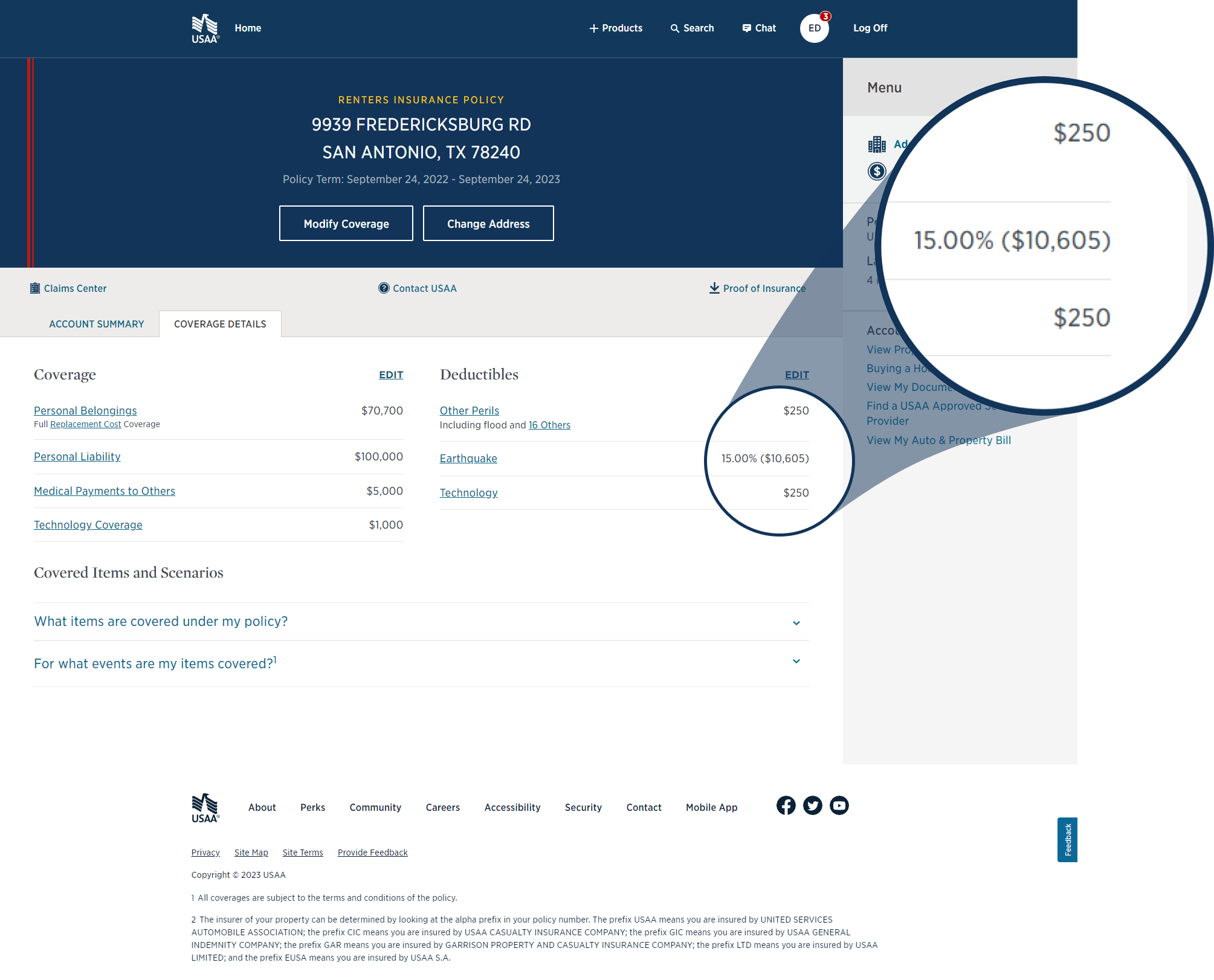

Q: Does my standard renters insurance cover earthquake damage? No. Most policies explicitly exclude earthquake-related losses. Tenants should confirm coverage limits or seek specialized rental insurance that fills this critical gap.

Q: What happens to my renters insurance after an earthquake? It typically pays for damaged personal property—your belongings lost or broken—but will not rebuild walls, foundations, or structural damage caused directly by quakes.

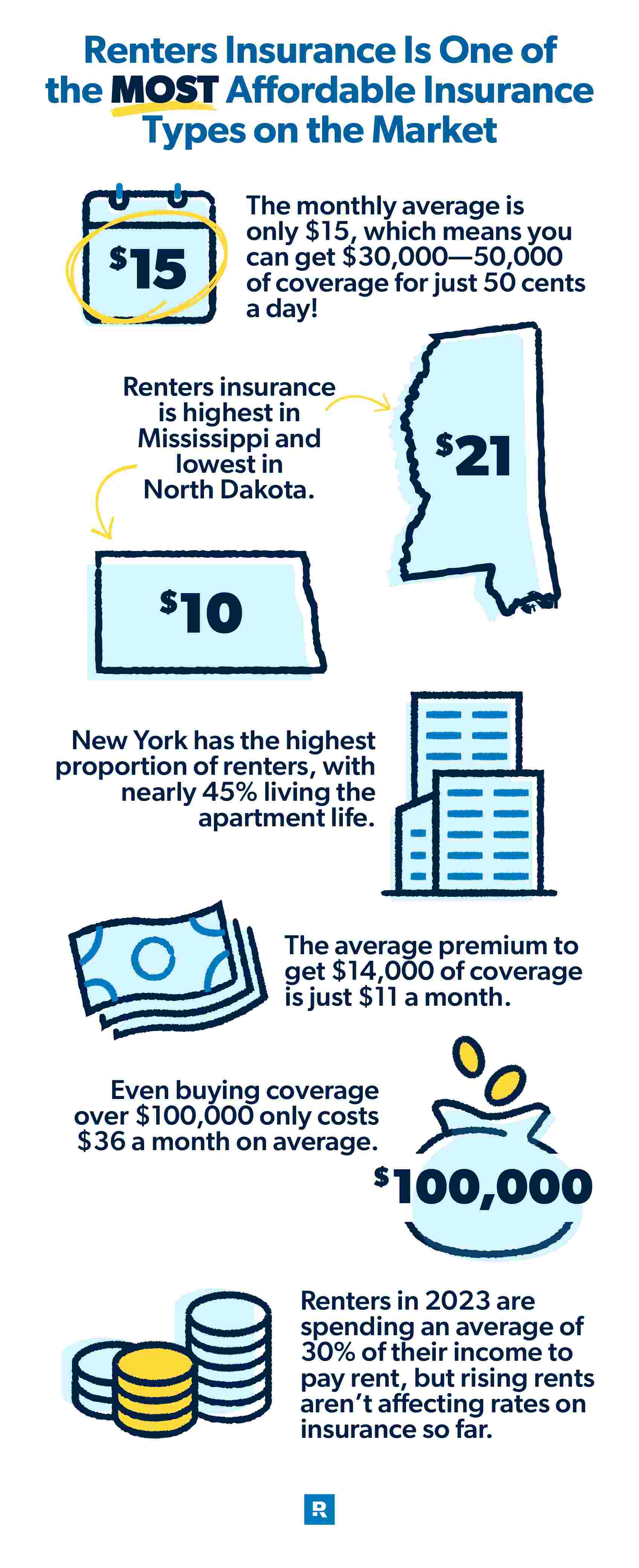

Q: Is earthquake coverage affordable for renters? Yes. Add-ons or standalone policies usually range from $10 to $50 per month—well below the potential replacement cost of a home’s contents and essential repairs.

Q: How often do earthquakes occur, and which U.S. states are most at risk? While major quakes are less frequent than other disasters, fault zones stretch across California, Washington, Oregon, Alaska, and parts of the Southeast. Even moderate tremors pose significant risk to renters nationwide.

Q: Can landlords cover earthquake damage for renters? Only in limited ways—often through building insurance or disclaimers. Most landlords do not provide personal rental insurance, leaving tenants solely responsible for their belongings. 7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes

Opportunities and Considerations

Addressing the earthquake gap offers both challenges and chance. For renters, increasing awareness opens doors to smarter decisions—protecting assets without overspending or panic-buying. For insurers, tailored products represent a growth frontier, though responsible pricing and clear communication remain vital.

There’s no perfect fix—earthquake insurance can’t replace public infrastructure investment—but informed renters gain leverage. Awareness drives demand, and demand attracts innovation. Closing the gap is not about fear, but preparation.

Things People Often Misunderstand

Many renters believe their standard policy fully covers unexpected damage, including earthquakes—this myth leaves thousands unprepared. Others assume renters insurance, like homeowners coverage, offers comprehensive protection.

The truth is clear: earthquake damage is excluded by design, not oversight. Tenants who act now avoid costly surprises. Hunting For Earthquake Coverage? Your Renters Insurance Is Cheating You Understanding exclusions isn’t about distrust—it’s about empowerment.

Who Earthquakes And Renters Insurance: The Dire Gap You Can’t Ignore Now May Be Relevant For

This gap affects city dwellers in seismic zones, especially renters in multifamily buildings. It matters to first-time renters, long-term tenants in older units, and urban renters nationwide facing increasing market volatility. Whether in Los Angeles,Chicago, or Nashville, the risk is real—what matters is readiness.

Beyond renters, this gap influences broader housing policy discussions, property investment strategies, and emergency planning at the community level. As housing insecurity rises and climate risks intensify, understanding and addressing this protection split becomes essential.

Soft CTA

If seismic risk weighs on your mind, take a mindful step: learn what your renters insurance covers—and what it doesn’t. Explore affordable coverage options, review your tenant agreements, and stay informed. Knowledge is your strongest defense.

Conclusion

Earthquakes And Renters Insurance: The Dire Gap You Can’t Ignore Now reveals a silent but urgent need—protection remains incomplete where it matters most. As tremors grow more frequent and urban life more concentrated, renters across the U.S. must recognize this vulnerability and act with clarity, not fear. By closing the gap through awareness and smart planning, families don’t just prepare for earthquakes—they secure peace of mind for what comes after.