Earthquake Coverage = Uninsured Nightmare Does Your Policy Have It? A growing concern in earthquake-prone regions, this phrase reflects a critical gap many U.S. homeowners and renters face—uninsured risks that can lead to financial devastation. As seismic activity increases across states like California, Oregon, and Washington, more people are asking: Do my current insurance policies cover earthquake damage? Hidden Risk Exposed: Renters Insurance Doesn't Cover Earthquakes × Here's What To Do The answer often surprises even the most cautious residents. With tremors capable of costing hundreds of thousands in repairs, the absence of proper earthquake coverage is increasingly viewed not just as a oversight—but a hidden financial threat.

---

Why Earthquake Coverage = Uninsured Nightmare Does Your Policy Have It? Is Gaining Attention Across the US

Recent years have seen rising awareness fueled by repeated strong quakes, media coverage, and community discussions. Hidden Risk Exposed: Renters Insurance Doesn't Cover Earthquakes × Here's What To Do As homes face stronger shaking than previously anticipated, insurance experts note a growing number of policyholders unknowingly lack protection. Digital tools and state-level disclosures now make risk transparency more accessible, pushing earthquake coverage to the forefront of household preparedness conversations. With the U.S. seismic risk expanding beyond traditional "Ring of Fire" areas, more people are recognizing that earthquakes are no longer rare—they’re inevitable. This shift in perception is turning what was once a niche concern into a mainstream insurance priority.

---

How Earthquake Coverage = Uninsured Nightmare Does Your Policy Have It? Must-Know Fact: Earthquakes Aren't Insured By Default × Insurance Lies You Don't Know Hidden Risk Exposed: Renters Insurance Doesn't Cover Earthquakes × Here's What To Do Actually Works

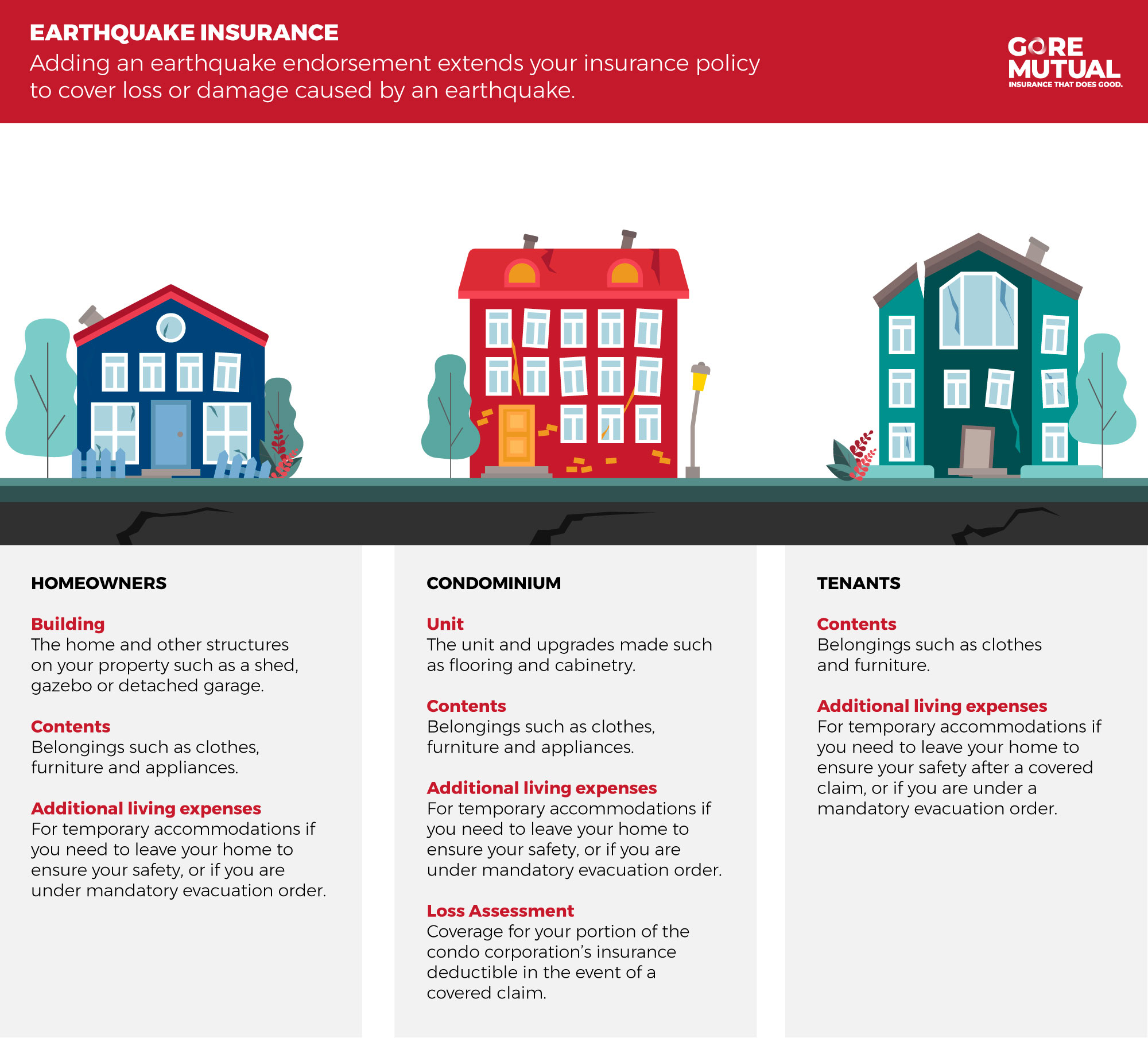

Earthquake coverage is designed to protect against structural damage caused by seismic events—cracks in foundations, broken plumbing, collapsed walls, and more—excluding contents like furniture or electronics. Unlike standard home insurance, which typically covers fire or wind-related damage, earthquake policies activate only after a qualifying seismic event. The coverage varies: some policies offer broad repair support, while others have coverage limits or deductibles specific to earthquake damage. Importantly, the absence of this protection means out-of-pocket costs can spike dramatically after a tremor. Having a clear, verified policy ensures predictable financial support when recovery is needed most. Start Now: How To Break Laser-Trained Aggression In Las Vegas Dogs

---

Common Questions People Have About Earthquake Coverage = Uninsured Nightmare Does Your Policy Have It?

Q: What does earthquake coverage actually pay for? A: It covers structural repairs triggered by seismic activity—such as foundation shifts, broken water lines, and damaged walls—provided they’re listed in your policy.

Q: Does renters insurance include earthquake coverage? A: Most standard renters policies exclude earthquake damage; a separate rider or standalone policy is typically needed for tenants.

Q: How much does earthquake coverage cost? A: Pricing varies based on location, home value, construction type, and coverage limits—typically ranging from 1% to 3% of your home’s value annually.

Q: What’s the difference between a deductible and a limit? A: The deductible is what you pay first before coverage starts; the limit caps the maximum payout for eligible earthquake-related repairs.

---

Opportunities and Considerations

Pros of Having Coverage: Peace of mind, predictable repair costs, and reduced financial stress after a disaster. Cons: Upfront costs, occasional deductibles, and policy exclusions require careful evaluation. Realistic Expectations: Earthquake coverage doesn’t cover all losses—understand what’s protected and what’s not.

---

Things People Often Misunderstand

Myth: Earthquake coverage isn’t necessary unless you live on the fault line. Reality: Tremors affect a wide area, and even moderate quakes can cause major damage far from the epicenter.

Myth: Standard home insurance includes earthquake protection. Fact: Most policies explicitly exclude seismic events—this is one of the most common coverage gaps.

Myth: A lower premium always means better value. Clarification: Lower costs may mean higher deductibles or limited coverage—balance matters.

---

Who Earthquake Coverage = Uninsured Nightmare Does Your Policy Have It? May Be Relevant For

This issue touches homeowners, renters, and buyers across earthquake-prone states: California, Oregon, Washington, parts of Nevada, and Colorado. Renters often overlook coverage since they own no structure—yet their belongings suffer damage too. First-time homeowners and fixers upgrading properties benefit from early coverage. Buyers should review seller disclosures—many property records now include seismic risk notes. Even renters relocating to high-risk zones should assess whether coverage is available or offered by third-party providers.

---

Soft CTA: Encourage Learning and Staying Informed

Don’t wait until the next tremor to ask whether your policy protects you. Use official resources like state insurance departments and trusted home repair guides to check coverage details before renewal. Understanding your earthquake risk—and having a plan—is a proactive step that pays in peace of mind. Stay informed, protect your future.

---

Conclusion Earthquake Coverage = Uninsured Nightmare Does Your Policy Have It? is more than a headline—it’s a critical checkpoint in household preparedness. With rising seismic risks and clearer data, the choice to protect is no longer optional. By understanding what your policy covers, correcting common misconceptions, and staying alert to your personal risk level, you empower yourself to face disasters with resilience, not fear. Knowledge is your strongest defense—before the ground shifts.