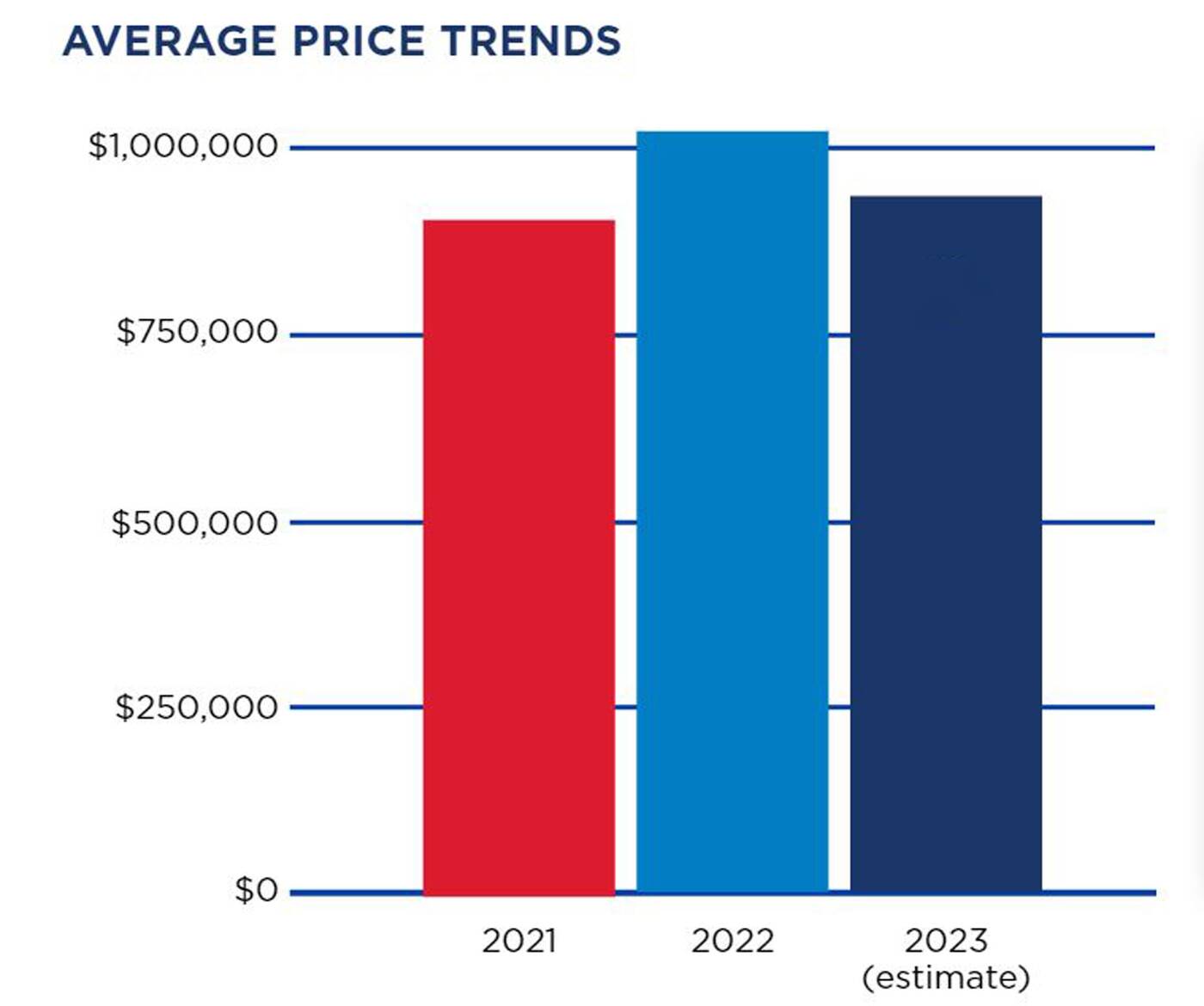

Atlanta Just $5,200 CheaperBut $9,400 Home Prices Make Reality Tougher

Why is a city once seen as more affordable now feeling financially out of reach? Atlanta, long celebrated for its accessibility and cultural vibrancy, is facing a growing disconnect between price expectations and current home values—just $5,200 cheaper upfront, but $9,400 more than many households’ budgets. This quiet shift isn’t just a local trend—it’s reshaping how Americans across the U.S. consider their housing options. Atlanta Only $6,500 Cheaper? This $6,800 Difference Will Shock Your Budget Plan With housing costs climbing steadily, Atlanta’s experience reflects a broader reality: proximity and promise now come with a steeper price tag that impacts first-time buyers, renters, and families alike.

Understanding the shift begins with a straightforward comparison: Atlanta home prices now sit roughly $9,400 above what many households can comfortably afford, despite the $5,200 savings at the point of purchase. This gap isn’t due to sudden market bubbles but reflects deeper economic pressures—rising construction costs, tighter inventory, and shifting workforce patterns driven by remote work. For those seeking value, the city remains attractive, yet affordability has become more fragile than ever.

The market dynamics behind Atlanta’s pricing challenge reveal a careful balancing act. Atlanta Only $6,500 Cheaper? This $6,800 Difference Will Shock Your Budget Plan While the upfront discount appears favorable, long-term affordability depends heavily on location, property type, and personal financial circumstances. Neighborhoods near major transit, schools, or employment hubs command higher premiums, narrowing the real benefit of lower initial costs. Buyers must weigh immediate savings against ongoing expenses, including property taxes, utilities, and maintenance—factors often hidden behind a flashy downpayment figure.

Common concerns include whether reduced initial costs translate into real savings over time and how Atlanta’s unique blend of urban appeal and rising prices affects long-term equity. These questions matter because they shape smart decisions in a market where appearances can be misleading. Atlanta Only $6,500 Cheaper? This $6,800 Difference Will Shock Your Budget Plan While affordable listing prices draw attention, sustained financial health depends on aligning expectations with realistic housing budgets.

A key misconception is assuming the $5,200 discount automatically eases homeownership. In reality, current prices $9,400 above average local income make traditional homeownership harder, especially for first-time buyers and middle-income families. Misreading short-term savings as long-term relief can lead to tougher financial choices down the line. Clear, data-driven awareness is essential.

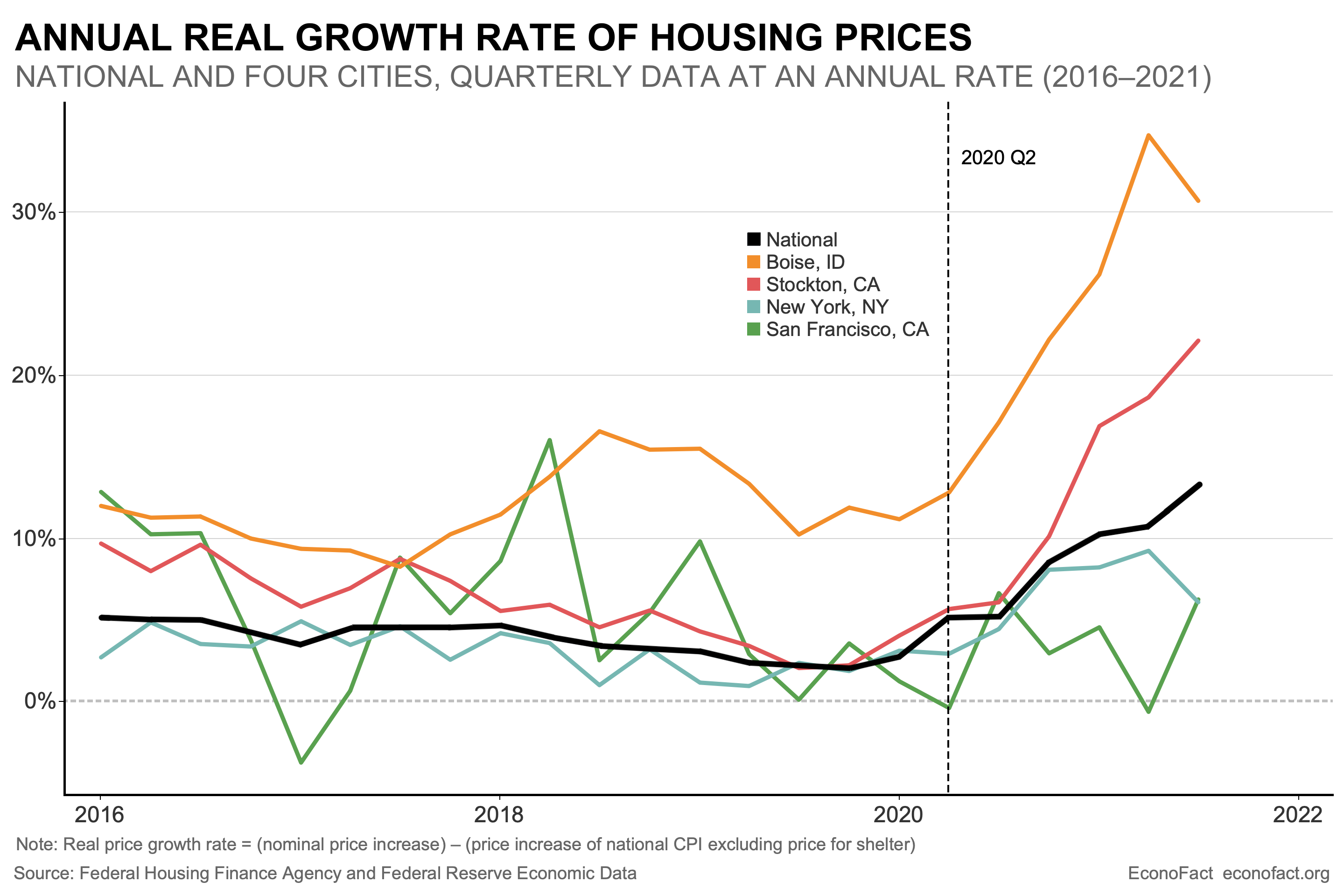

Housing trends in Atlanta mirror national patterns: urban centers offer opportunity but at a cost many can scarcely meet. For mobile-first, information-driven users navigating real estate today, awareness of these nuances builds stronger confidence—transforming curiosity into informed action.

Beyond immediate concerns, Atlanta’s market signals evolving opportunities: targeted financing options, emerging neighborhoods, and tech tools helping buyers analyze value beyond sticker price. These trends support smarter, more strategic decisions, helping users align choices with long-term goals.

In a landscape where perception shapes action, Atlanta’s story—just $5,200 cheaper upfront but $9,400 more costly over time—urges readers to look deeper than first look. Understanding local economics, personal finance, and market dynamics helps create meaningful, sustainable homeownership journeys. By turning curiosity into clarity, readers gain not just insight—but confidence—in navigating one of the U.S.’s most dynamic housing markets.