7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes

Why are so many renters surprised—and concerned—when a property policy fails to cover seismic damage? For decades, rental insurance has been seen as a straightforward shield for everyday risks. But when an earthquake strikes, reality shifts—often invisibly, and always significantly. Earthquakes And Renters Insurance: The Dire Gap You Can't Ignore Now The truth is, standard renters insurance never includes earthquake protection. Here are 7 shocking truths every renter should know before disaster strikes.

Why 7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes Is Gaining Attention in the US

As natural disaster frequency rises and climate uncertainty grows, rental owners across the country are noticing a glaring gap in protection. Renters Insurance, designed to cover fire, wind, theft, and water damage, deliberately excludes earthquake risks—leaving many to face massive unexpected costs. Earthquakes And Renters Insurance: The Dire Gap You Can't Ignore Now Social media discussions, homeowner forums, and insurance advisory groups have seen a sharp uptick in questions, driven by real estate shifts and rising quake zones in states like California, Oregon, and Washington. The lack of transparency around this exclusion fuels confusion, making it more critical than ever to uncover the hidden risks behind your policy letter.

How 7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes Actually Works

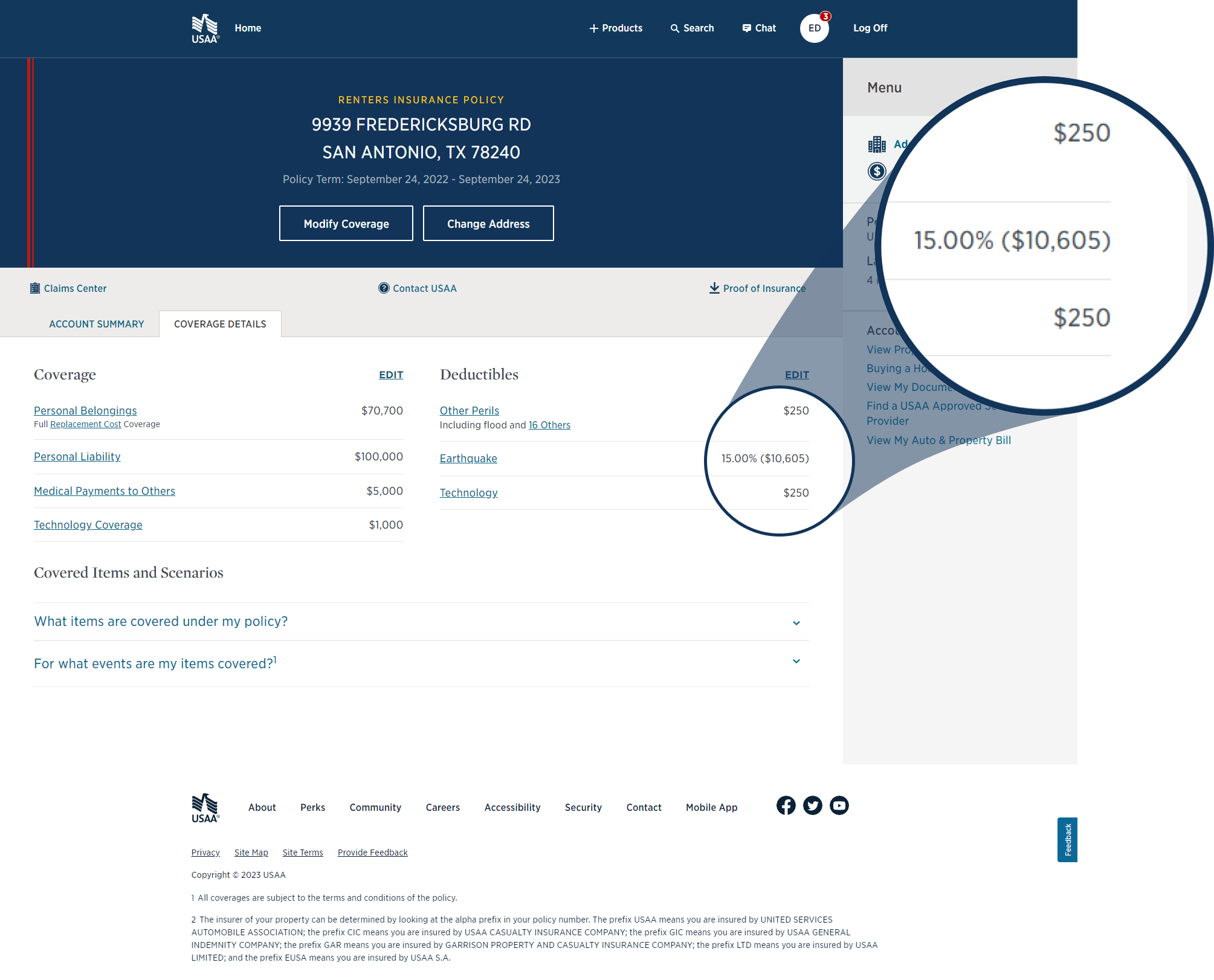

Unlike standard coverage that kicks in automatically, earthquake damage typically requires a supplemental policy. Renters insurance usually limits coverage for non-weather-related structural damage—earthquakes fall squarely into this category. Earthquakes And Renters Insurance: The Dire Gap You Can't Ignore Now Insurers exclude earthquake risks because seismic events cause sudden, widespread damage to foundations, walls, plumbing, and appliances. Even small tremors can trigger costly repairs beyond typical coverage limits. When a claim is filed, insurers evaluate whether the damage qualifies as structural collapse—standard policy terms often deny or limit payouts unless specific earthquake add-ons are purchased. This exclusion protects insurers from unpredictable, high-severity events, but leaves renters financially vulnerable if unprepared.

Common Questions People Have About 7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes

Q: What exactly is excluded? A: Structural damage from seismic activity—such as cracked foundations, shifted walls, or broken plumbing—unless covered by an endorsement. Normal wear and tear aren’t the issue; sudden tectonic stress is.

Q: Can I add earthquake coverage later? A: Yes, it’s possible through specialized policies or riders, but coverage is available only after purchase and depends on location, risk assessment, and premium costs.

Q: Do all homeowners or renters need it? A: Only renters in seismically active zones should seriously consider supplemental protection. Standard insurance excludes earthquakes nationwide for renters regardless of location, though risk varies.

Q: Is earthquake damage ever covered without a separate policy? A: Extremely limited. Some rental units with older construction may offer minimal coverage, but this depends on property age and insurer terms—never assume automatic protection.

Q: How long does it take to file a claim? A: Claims vary—speed depends on damage severity, documentation, and insurer responsiveness, but prompt action is critical to maximize coverage.

Q: Are rental property modifications considered? A: Yes. Add-ons often require proof of seismic-safe upgrades. Insurers evaluate structural resilience before confirming coverage.

Q: Can renters store earthquake insurance alongside renters policy? A: Yes, but bundling adds cost. Separate policies mean paying for duplication, so assess risk vs. budget before deciding. Hunting For Earthquake Coverage? Your Renters Insurance Is Cheating You

Opportunities and Considerations

Pros of Knowing the Truth Now Understanding what’s not covered prevents costly surprises during disaster recovery. Proactive steps—like evaluating location risk and exploring supplemental coverage—build long-term resilience. Renters gain clarity to plan wisely and avoid policy blind spots.

Cons and Realistic Expectations There’s no free earthquake protection built into standard renters insurance. Expanding coverage increases premiums, and policy terms vary widely. Renter mindfulness about seismic zones and property history remains key.

Things People Often Misunderstand

- Earthquakes aren’t just for “fault lines”—reactive ground shaking can damage homes far from active faults. - Insurance exclusions are standard, not a policy flaw—they reflect actuarial risk, not neglect. - A single seismic event can ruin a unit irreparably; prevention isn’t affordable at scale. - Rental property age affects risk—newer construction may meet modern safety codes, lowering exposure.

Who 7 Shocking Truths Renters Insurance Does NOT Cover Earthquakes May Be Relevant For

This insight matters to renters in earthquake-prone regions—particularly along the West Coast and in parts of the Midwest facing emerging seismic activity. First-time renters buying property in known fault zones should ask agents about seismic coverage. Property managers in high-risk cities can integrate this knowledge into lease terms and tenant education. Renters in older buildings or coastal cities with underground faults benefit most from evaluating their protection gaps early.

Soft CTA Staying informed is your best defense. Explore how supplemental earthquake coverage fits into your long-term home protection plan—no pressure, just clarity. Research local seismic risks, consult trusted inspectors, and ask insurers about tailored add-ons that align with your location and budget. Knowledge allows smarter, calmer decisions when peace of mind matters most.

Conclusion The truth about renters insurance and earthquakes isn’t dramatic—it’s practical. Seven shocking realities reveal a critical gap: most policies exclude seismic damage by design. By understanding this early, renters across the U.S.—especially in vulnerable areas—can protect their investments and futures with confidence. Informed choices today lead to greater resilience tomorrow.